Question: Consider a stock priced at $30 with a standard deviation of 3. The risk-free rate is .05. There are put and call options available at

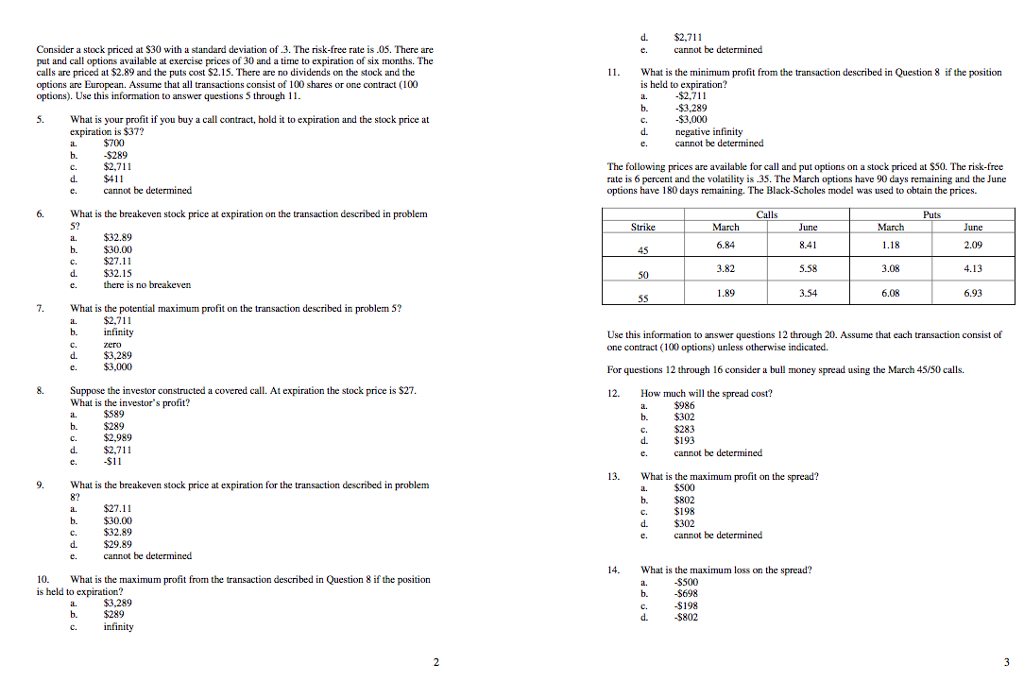

Consider a stock priced at $30 with a standard deviation of 3. The risk-free rate is .05. There are put and call options available at exercise prices of 30 and a time to expiration of six months. The calls are priced at $2.89 and the puts cost $2.15. There are no dividends on the stock and the options are European. Assume that all transactions consist of 100 shares or one contract (100 options). Use this information to answer questions 5 through 11 cannot be determined 11. What is the minimum profit from the transaction described in Question 8 if the position is held to expiration? a. $2.711 $3,289 5 What is your profit if you buy a cal contract, hold it to expiration and the stock price at c. $3.000 expiration is $37? d. negative infinity e. cannot be determined b. 289 $2,711 $411 cannot be determined The following prices are available for call and put options on a stock priced at $50. The risk-free rate is 6 percent and the volatility is 35. The March options have 90 days remaining and the June options have 180 days remaining. The Black-Scholes model was used to obtain the prices. c. d. 6. What is the breakeven stock price at expiration on the transationdescribed in problem Calls 52 a $32.89 b. $30.00 March 6.84 3.82 1.89 March 8.41 5.58 3.54 2.09 $27.11 $32.15 there is no breakeven 3.08 d. 6.08 6.93 What is the potential maximum profit on the transaction described in problem 5? a $2,711 b. infinity Use this information to answer questions 12 through 20. Assume that each transaction consist of one contract (100 options) unless otherwise indicated For questions 12 through 16 consider a bull money spread using the March 45/S0 calls. 12. How much will the spread cost? d. e. ero $3,289 $3,000 8. Suppose the investor constructed a covered call. At expiration the stock price is $27 What is the investor's profit? b. c. d. $289 $2,989 $2,711 a. 986 b. $302 . $283 d. $193 e. cannot be determined 13. What is the maximum profit on the spread? a. S500 b. $802 . $198 d 302 e. cannot be determined 9 What is the breakeven stock price at expiration for the transaction described in problem 8? a $27.11 b. $30.00 c. S32.89 d. $29.89 e. cannot be determined 14. What is the maximum loss on the spread? 0. What is the maximum profit from the transaction described in Question 8 if the position is held to expiration? $500 b. 698 c. $198 d. $802 b. $289 infinity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts