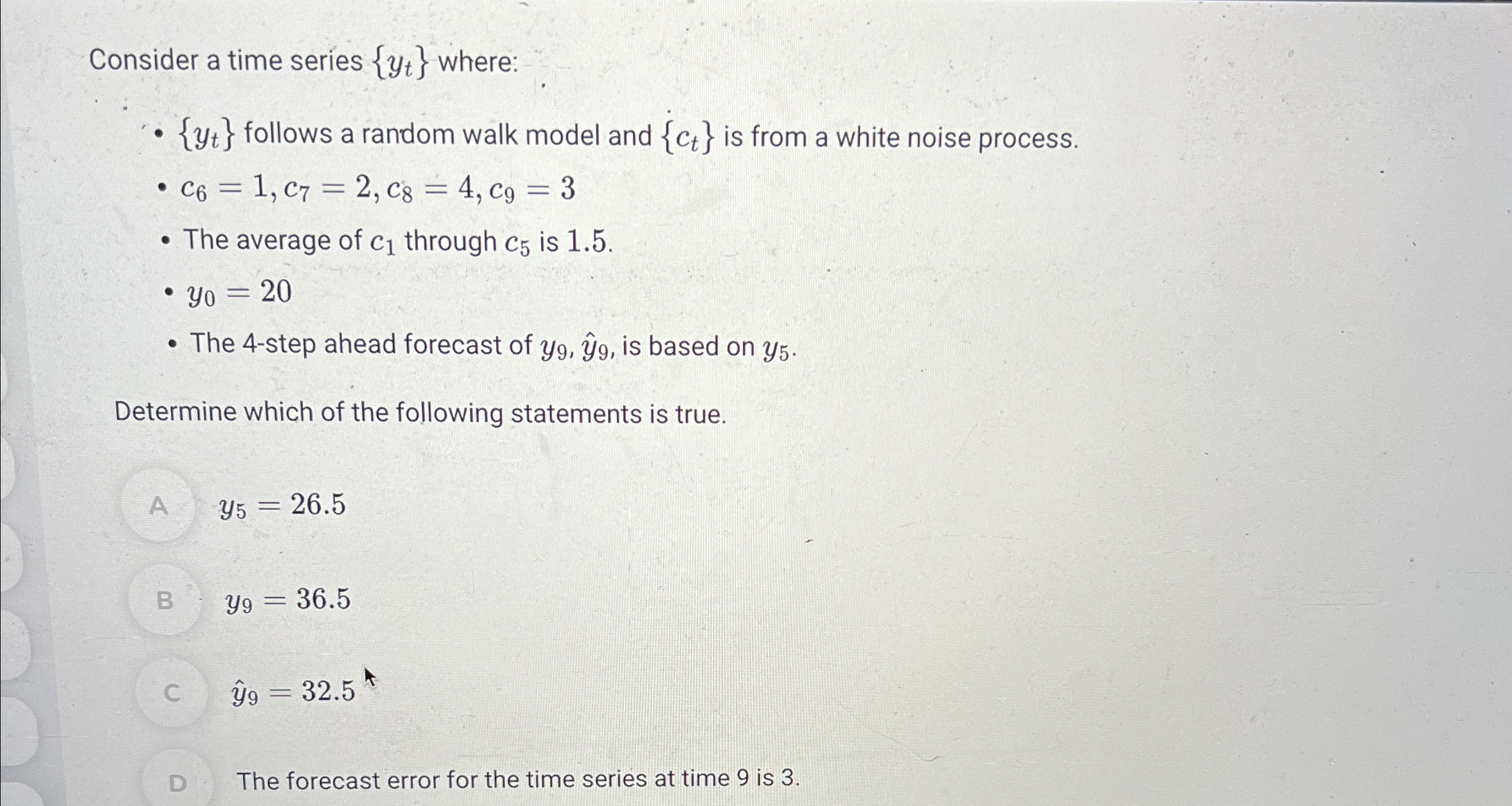

Question: Consider a time series { y t } where: { y t } follows a random walk model and { c t } is from

Consider a time series where:

follows a random walk model and is from a white noise process.

The average of through is

The step ahead forecast of hat is based on

Determine which of the following statements is true.

hat

The forecast error for the time series at time is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock