Question: Consider a two - period securities market model, with two risky securities S 1 , S 2 . The dynamics of the price processes (

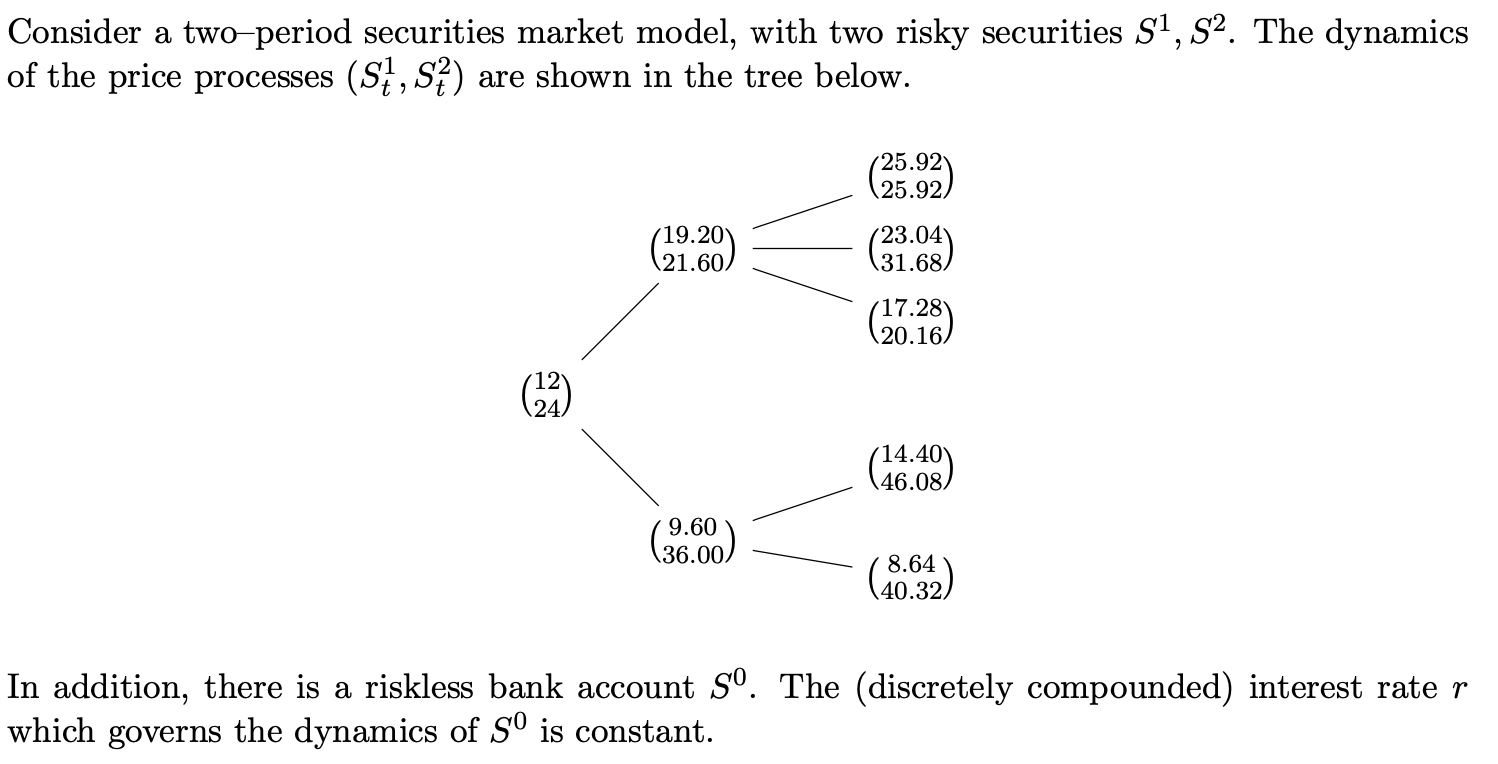

Consider a twoperiod securities market model, with two risky securities The dynamics of the price processes are shown in the tree below.

In addition, there is a riskless bank account The discretely compounded interest rate

which governs the dynamics of is constant.

a Show that the model is indeed arbitragefree by finding an EMM for this model.

b Is this model complete? Why or why not?

c Consider a chooser option X on S which allows the holder to decide, at time t whether the option is a call on S with strike K and maturity T or a put with strike K and maturity T What are the t and t prices of this option?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock