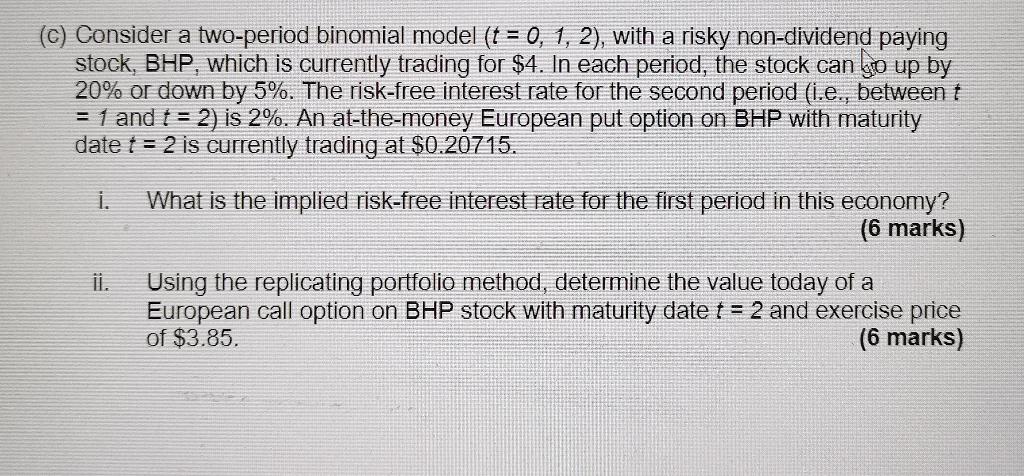

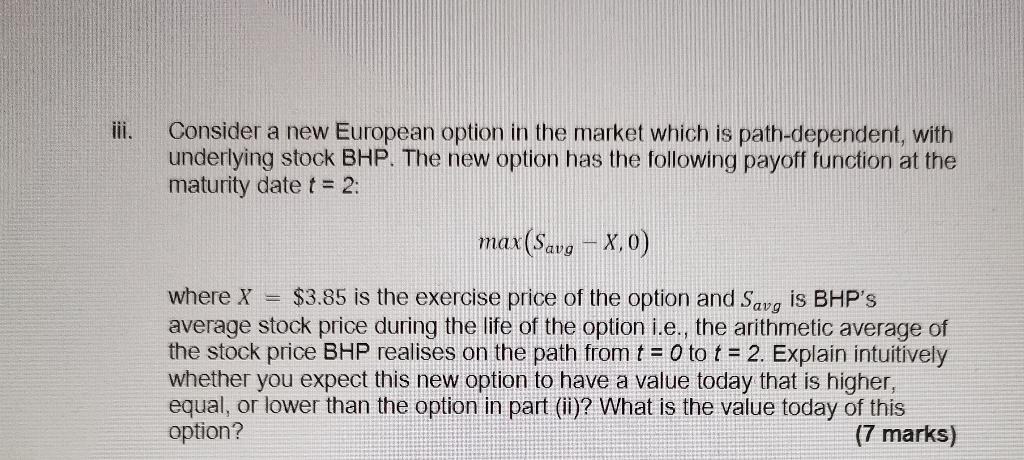

Question: () Consider a two-period binomial model (t = 0, 1, 2), with a risky non-dividend paying stock, BHP, which is currently trading for $4. In

() Consider a two-period binomial model (t = 0, 1, 2), with a risky non-dividend paying stock, BHP, which is currently trading for $4. In each period, the stock can ko up by 20% or down by 5%. The risk-free interest rate for the second period (i.e., between t = 1 and t = 2) is 2%. An at-the-money European put option on BHP with maturity date t = 2 is currently trading at $0.20715. i. What is the implied risk-free interest rate for the first period in this economy? (6 marks) ii. Using the replicating portfolio method, determine the value today of a European call option on BHP stock with maturity date t = 2 and exercise price of $3.85. (6 marks) Consider a new European option in the market which is path-dependent, with underlying stock BHP. The new option has the following payoff function at the maturity date t = 2: max(Savg X,0) where x = $3.85 is the exercise price of the option and Savg is BHP's average stock price during the life of the option i.e., the arithmetic average of the stock price BHP realises on the path from t = 0 to t = 2. Explain intuitively whether you expect this new option to have a value today that is higher, equal, or lower than the option in part (ii)? What is the value today of this option? (7 marks) () Consider a two-period binomial model (t = 0, 1, 2), with a risky non-dividend paying stock, BHP, which is currently trading for $4. In each period, the stock can ko up by 20% or down by 5%. The risk-free interest rate for the second period (i.e., between t = 1 and t = 2) is 2%. An at-the-money European put option on BHP with maturity date t = 2 is currently trading at $0.20715. i. What is the implied risk-free interest rate for the first period in this economy? (6 marks) ii. Using the replicating portfolio method, determine the value today of a European call option on BHP stock with maturity date t = 2 and exercise price of $3.85. (6 marks) Consider a new European option in the market which is path-dependent, with underlying stock BHP. The new option has the following payoff function at the maturity date t = 2: max(Savg X,0) where x = $3.85 is the exercise price of the option and Savg is BHP's average stock price during the life of the option i.e., the arithmetic average of the stock price BHP realises on the path from t = 0 to t = 2. Explain intuitively whether you expect this new option to have a value today that is higher, equal, or lower than the option in part (ii)? What is the value today of this option? (7 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts