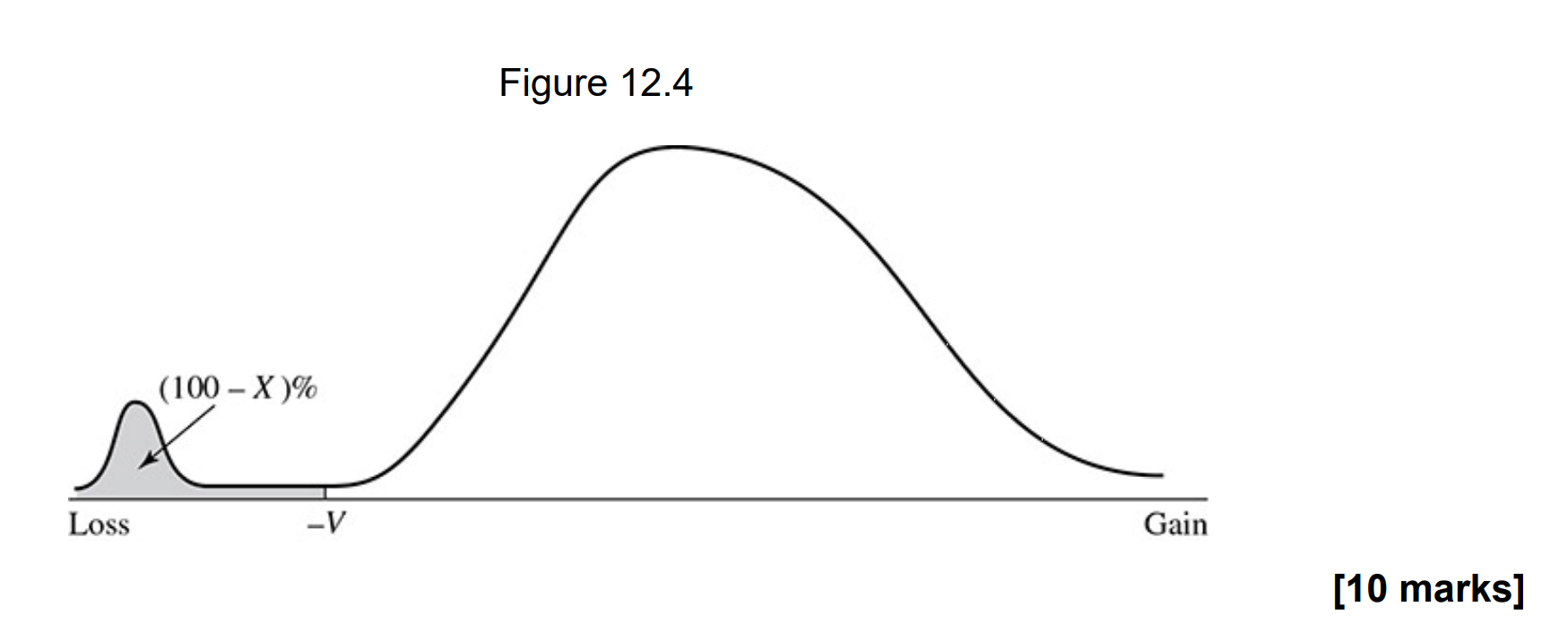

Question: Consider figure 12.4 below from the Hull book. It is the probability distribution for gain in portfolio value during time T and at confidence level

Consider figure 12.4 below from the Hull book. It is the probability distribution for gain in portfolio value during time T and at confidence level X%. Discuss the pitfalls of using VaR at level V. Would you recommend another risk measure? If yes, discuss the tradeoff between VaR and this other risk measure.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock