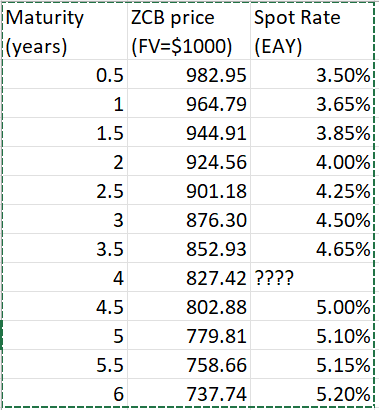

Question: Consider the attached spreadsheet with U . S . Treasury zero - coupon bond prices. The face values are equal to $ 1 , 0

Consider the attached spreadsheet with US Treasury zerocoupon bond prices. The face values are equal to $

a What is the annual fouryear riskfree spot rate?

b What is the current fair price of a US Treasury coupon bond with face value $ years to maturity, annual coupon rate of and paying semiannual coupons?

c What is the current fair yieldtomaturity of the coupon bond in the previous question US Treasury coupon bond with face value $ years to maturity, annual coupon rate of and paying semiannual coupons

d Consider a bond like that of two questions ago US Treasury coupon bond with face value $ years to maturity, annual coupon rate of and paying semiannual coupons Assume you are a bond dealer facing negligible transaction costs. What would you do if the market price of the bond was equal to $

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock