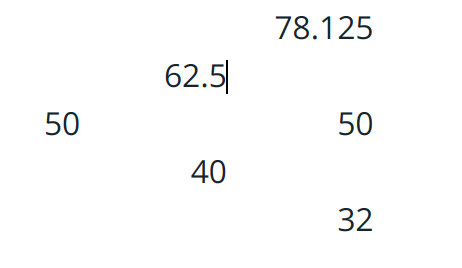

Consider the following binomial tree, a risk-free rate is 8% per annum with continuous compounding, each step

Fantastic news! We've Found the answer you've been seeking!

Question:

Consider the following binomial tree, a risk-free rate is 8% per annum with continuous compounding, each step represents a period of 3 months, and the relevant strike price is 55.

Question 1. What is the risk-neutral probability of an increase or decrease in the price of the stock, respectively?

Question 2. Considering the data mentioned in the context, what is the number of shares of the replicating portfolio, for C+?

Question 3. Considering the data mentioned in the context, the value of a European call option with a strike of 55 and a time to maturity of 6 months is?

Expert Answer:

1 The riskneutral probability of an increase or decrease in the price of the stock can be calculated ... View the full answer

Related Book For

Posted Date: