Question: Consider the following CDO transaction: 1. The CDO is a $200 million structure. That is, the assets purchased will be $200 million. 2. The collateral

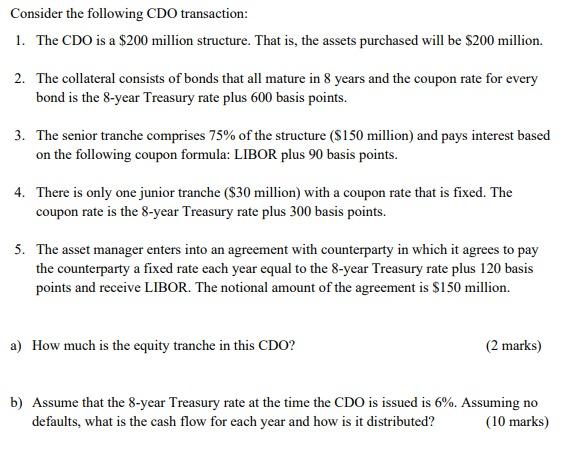

Consider the following CDO transaction: 1. The CDO is a $200 million structure. That is, the assets purchased will be $200 million. 2. The collateral consists of bonds that all mature in 8 years and the coupon rate for every bond is the 8-year Treasury rate plus 600 basis points. 3. The senior tranche comprises 75% of the structure ($150 million) and pays interest based on the following coupon formula: LIBOR plus 90 basis points. 4. There is only one junior tranche ($30 million) with a coupon rate that is fixed. The coupon rate is the 8-year Treasury rate plus 300 basis points. 5. The asset manager enters into an agreement with counterparty in which it agrees to pay the counterparty a fixed rate each year equal to the 8-year Treasury rate plus 120 basis points and receive LIBOR. The notional amount of the agreement is $150 million. a) How much is the equity tranche in this CDO? (2 marks) b) Assume that the 8-year Treasury rate at the time the CDO is issued is 6%. Assuming no defaults, what is the cash flow for each year and how is it distributed? (10 marks) Consider the following CDO transaction: 1. The CDO is a $200 million structure. That is, the assets purchased will be $200 million. 2. The collateral consists of bonds that all mature in 8 years and the coupon rate for every bond is the 8-year Treasury rate plus 600 basis points. 3. The senior tranche comprises 75% of the structure ($150 million) and pays interest based on the following coupon formula: LIBOR plus 90 basis points. 4. There is only one junior tranche ($30 million) with a coupon rate that is fixed. The coupon rate is the 8-year Treasury rate plus 300 basis points. 5. The asset manager enters into an agreement with counterparty in which it agrees to pay the counterparty a fixed rate each year equal to the 8-year Treasury rate plus 120 basis points and receive LIBOR. The notional amount of the agreement is $150 million. a) How much is the equity tranche in this CDO? (2 marks) b) Assume that the 8-year Treasury rate at the time the CDO is issued is 6%. Assuming no defaults, what is the cash flow for each year and how is it distributed? (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts