Question: Consider the following equation: t + 1 = ayt + (1 - a) >t Where: t + 1 = forecast of the time series for

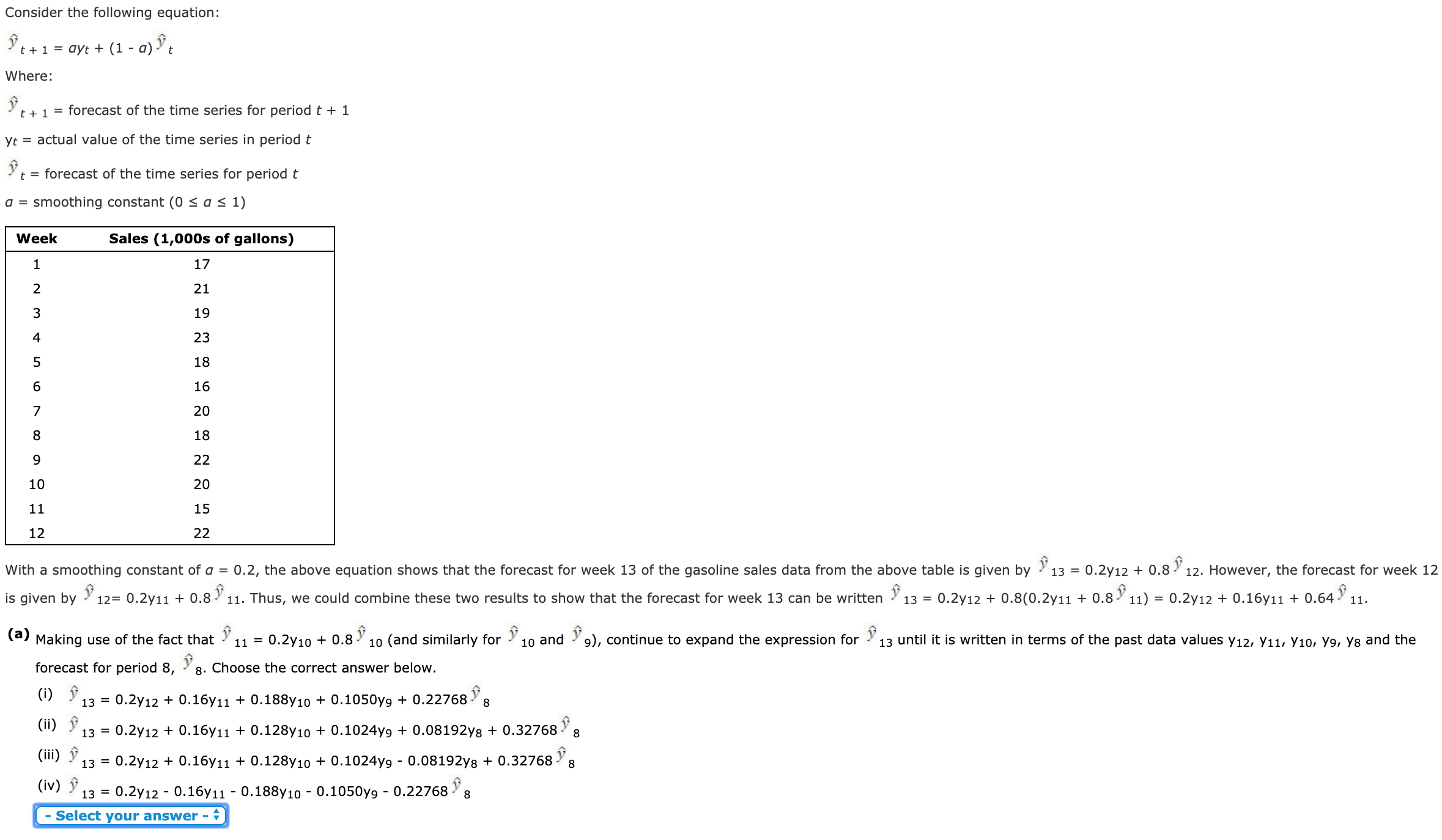

Consider the following equation: t + 1 = ayt + (1 - a) >t Where: t + 1 = forecast of the time series for period t + 1 yt = actual value of the time series in period t 't = forecast of the time series for period t a = smoothing constant (0 s a s 1) Week Sales (1,000s of gallons) 1 17 5 6 0 V A UT A W N 21 19 23 18 16 20 18 22 20 15 12 22 With a smoothing constant of a = 0.2, the above equation shows that the forecast for week 13 of the gasoline sales data from the above table is given by 13 = 0.2y12 + 0.8 12. However, the forecast for week 12 is given by 12= 0.2y11 + 0.8 11. Thus, we could combine these two results to show that the forecast for week 13 can be written 13 = 0.2y12 + 0.8(0.2y11 + 0.8 11) = 0.2y12 + 0.16y11 + 0.64 ) 11. () Making use of the fact that 11 = 0.2y10 + 0.8 10 (and similarly for 10 and 9), continue to expand the expression for 13 until it is written in terms of the past data values y12, Y11, y10, 19, y: and the forecast for period 8, 8. Choose the correct answer below. () 13 = 0.2y12 + 0.16/11 + 0.188/10 + 0.1050yg + 0.22768 : (ii) 13 = 0.2y12 + 0.1611 + 0.12810 + 0.1024y9 + 0.08192yg + 0.32768 8 (iii) y 13 = 0.2y12 + 0.16y11 + 0.12810 + 0.10249 - 0.08192yg + 0.32768 : (iv) y 13 = 0.2y12 - 0.16y11 - 0.188y10 - 0.1050y9 - 0.22768 8 - Select your

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts