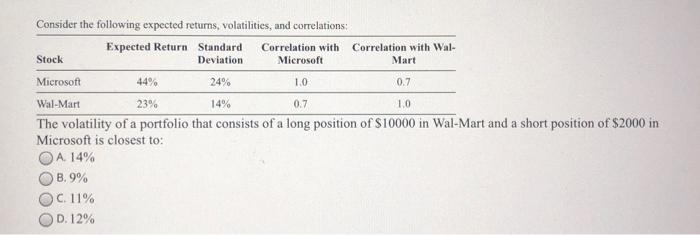

Question: Consider the following expected returns, volatilities, and correlations: Expected Return Standard Correlation with Correlation with Wal- Stock Deviation Microsoft Mart Microsoft 44% 24% 1.0 0.7

Consider the following expected returns, volatilities, and correlations: Expected Return Standard Correlation with Correlation with Wal- Stock Deviation Microsoft Mart Microsoft 44% 24% 1.0 0.7 23% 14% 0.7 1.0 Wal-Mart The volatility of a portfolio that consists of a long position of $10000 in Wal-Mart and a short position of $2000 in Microsoft is closest to: A 14% B.9% C. 11% OD. 12%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock