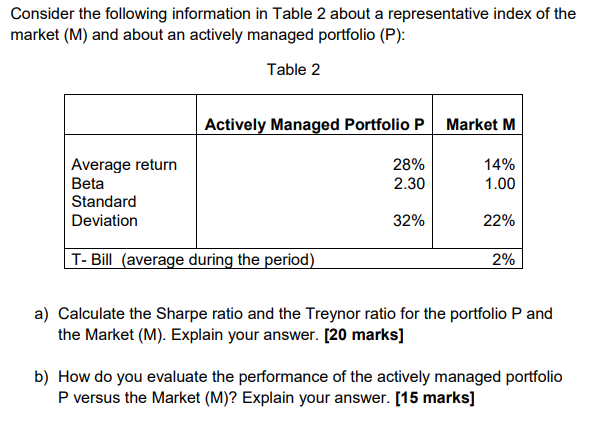

Question: Consider the following information in Table 2 about a representative index of the market (M) and about an actively managed portfolio (P): Table 2 Actively

Consider the following information in Table 2 about a representative index of the market (M) and about an actively managed portfolio (P): Table 2 Actively Managed Portfolio P Market M 28% 2.30 14% 1.00 Average return Beta Standard Deviation 32% 22% T- Bill (average during the period) 2% a) Calculate the Sharpe ratio and the Treynor ratio for the portfolio P and the Market (M). Explain your answer. [20 marks] b) How do you evaluate the performance of the actively managed portfolio P versus the Market (M)? Explain your answer. [15 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock