Question: Consider the following information regarding corporate bonds: Rating Average Default Rate Recession Default Rate Average Beta A 0.2% 3.0% 0.05 BBB 0.45% 3.0% 0.10 2.2%

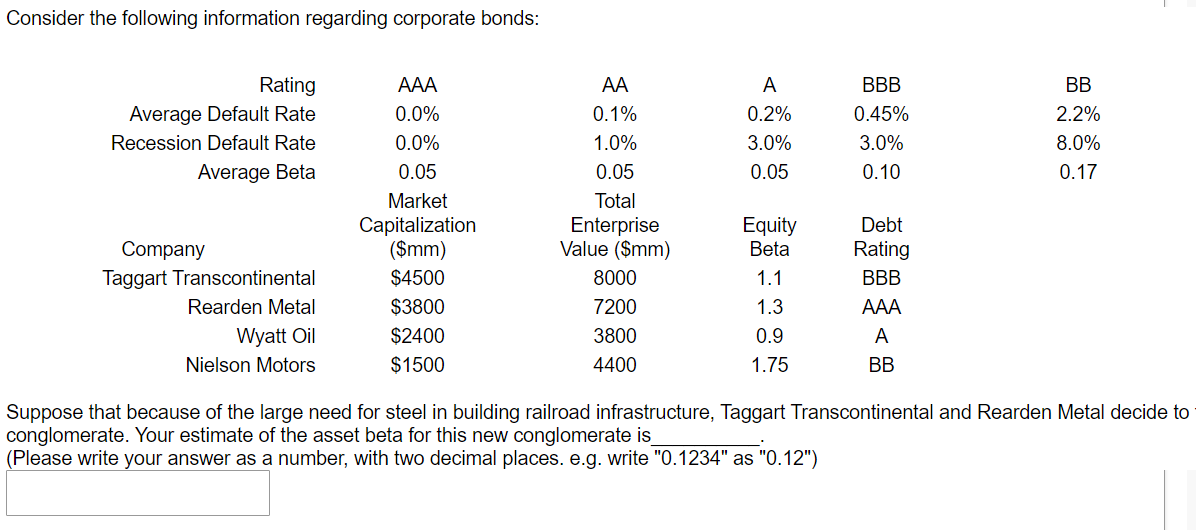

Consider the following information regarding corporate bonds: Rating Average Default Rate Recession Default Rate Average Beta A 0.2% 3.0% 0.05 BBB 0.45% 3.0% 0.10 2.2% 8.0% 0.17 AAA 0.0% 0.0% 0.05 Market Capitalization ($mm) $4500 $3800 $2400 $1500 AA 0.1% 1.0% 0.05 Total Enterprise Value ($mm) 8000 7200 3800 4400 Company Taggart Transcontinental Rearden Metal Wyatt Oil Nielson Motors Equity Beta 1.1 1.3 0.9 1.75 Debt Rating BBB AAA A BB Suppose that because of the large need for steel in building railroad infrastructure, Taggart Transcontinental and Rearden Metal decide to conglomerate. Your estimate of the asset beta for this new conglomerate is (Please write your answer as a number, with two decimal places. e.g. write "0.1234" as "0.12")

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts