Question: Consider the following multifactor (APT) model of security returns for a particular stock. Factor Factor Beta Factor Risk Premium Inflation 1.07 0.06 Industrial production 0.49

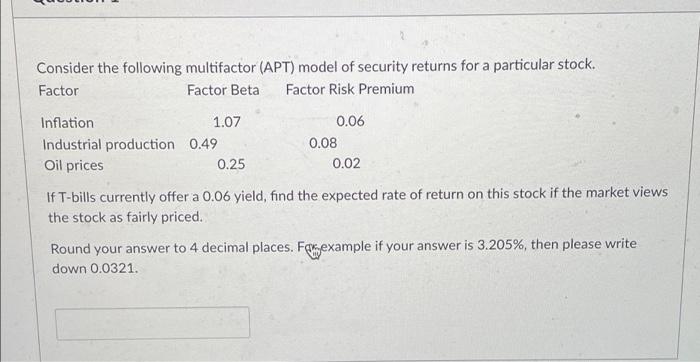

Consider the following multifactor (APT) model of security returns for a particular stock. Factor Factor Beta Factor Risk Premium Inflation 1.07 0.06 Industrial production 0.49 0.08 Oil prices 0.25 0.02 If T-bills currently offer a 0.06 yield, find the expected rate of return on this stock if the market views the stock as fairly priced. Round your answer to 4 decimal places. Fakexample if your answer is 3.205%, then please write down 0.0321

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock