Question: Consider the following returns for Security J, Security K, and the Market: Year Security J Security K Market 110%12%6%214%8%10%312%16%14%48%10%4%520%22%16% Assume that expected returns are modeled

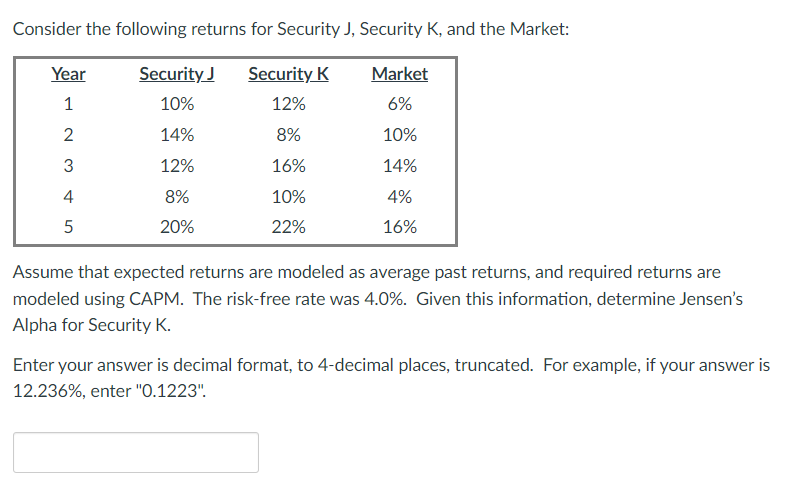

Consider the following returns for Security J, Security K, and the Market:

YearSecurity JSecurity KMarket110%12%6%214%8%10%312%16%14%48%10%4%520%22%16%

Assume that expected returns are modeled as average past returns, and required returns are modeled using CAPM. The risk-free rate was 4.0%. Given this information, determine Jensens Alpha for Security K.

Enter your answer is decimal format, to 4-decimal places, truncated. For example, if your answer is 12.236%, enter "0.1223".

Consider the following returns for Security J, Security K, and the Market: Assume that expected returns are modeled as average past returns, and required returns are modeled using CAPM. The risk-free rate was 4.0\\%. Given this information, determine Jensen's Alpha for Security K. Enter your answer is decimal format, to 4-decimal places, truncated. For example, if your answer is 12.236\\%, enter \"0.1223\". Consider the following returns for Security J, Security K, and the Market: Assume that expected returns are modeled as average past returns, and required returns are modeled using CAPM. The risk-free rate was 4.0\\%. Given this information, determine Jensen's Alpha for Security K. Enter your answer is decimal format, to 4-decimal places, truncated. For example, if your answer is 12.236\\%, enter \"0.1223\

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts