Question: Consider the following structural VAR model Y2t = = 10 312 2,111,t-1 +122,-1+1,t 20 321 1,211,t-1 +22 2,t-1+2, - where (1)~d Questions: (1) Write

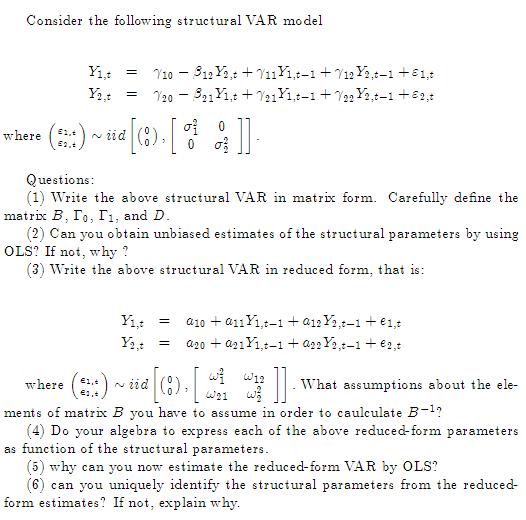

Consider the following structural VAR model Y2t = = 10 312 2,111,t-1 +122,-1+1,t 20 321 1,211,t-1 +22 2,t-1+2, - where (1)~d Questions: (1) Write the above structural VAR in matrix form. Carefully define the matrix B, To, T, and D.. (2) Can you obtain unbiased estimates of the structural parameters by using OLS? If not, why? (3) Write the above structural VAR in reduced form, that is: Yt = Yt = a10a111,-1+ a12 Y2,-1 + 1,t a20 + a211,-1+ a22 Y2,-1 + 2,t where ()~iid [() [ w W12 We w ]] What assumptions about the ele- ments of matrix B you have to assume in order to caulculate B-? (4) Do your algebra to express each of the above reduced-form parameters as function of the structural parameters. (5) why can you now estimate the reduced-form VAR by OLS? (6) can you uniquely identify the structural parameters from the reduced- form estimates? If not, explain why.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts