Question: Consider the following trading and performance data for four different equity mutual funds: a. Calculate the portfolio turnover ratio for each fund. Do not round

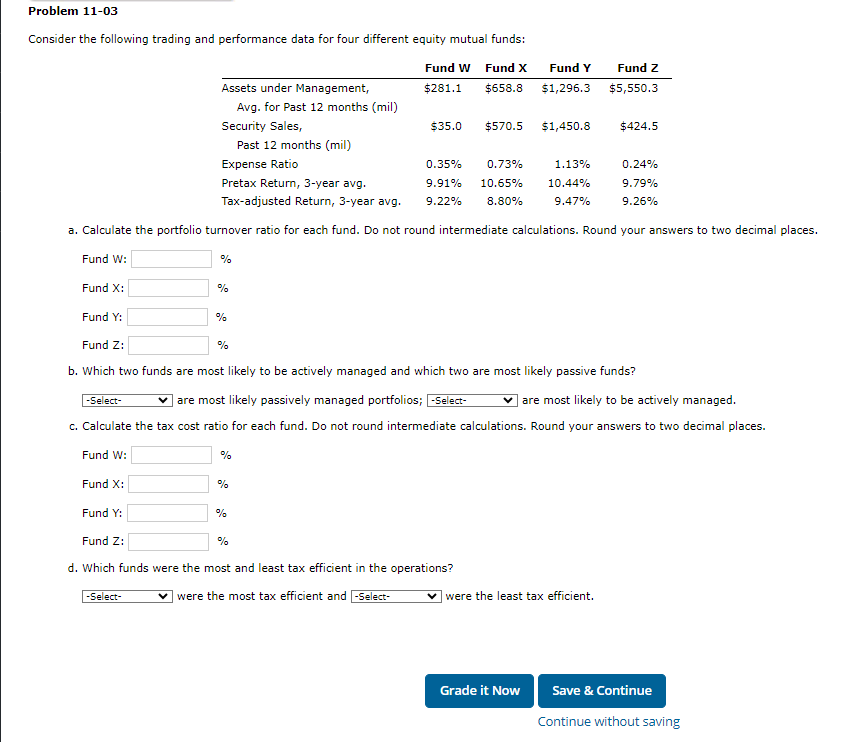

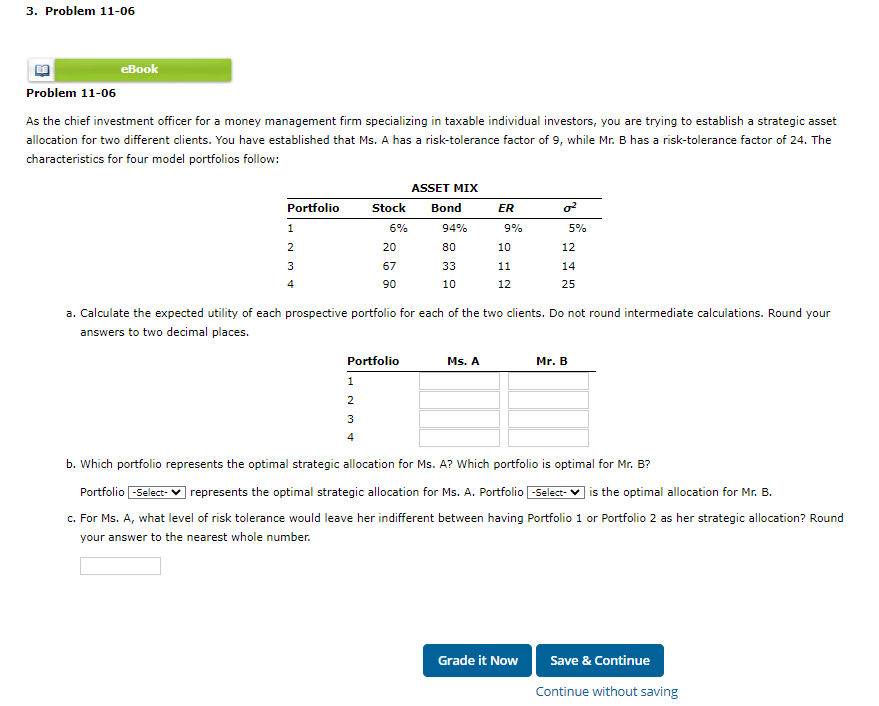

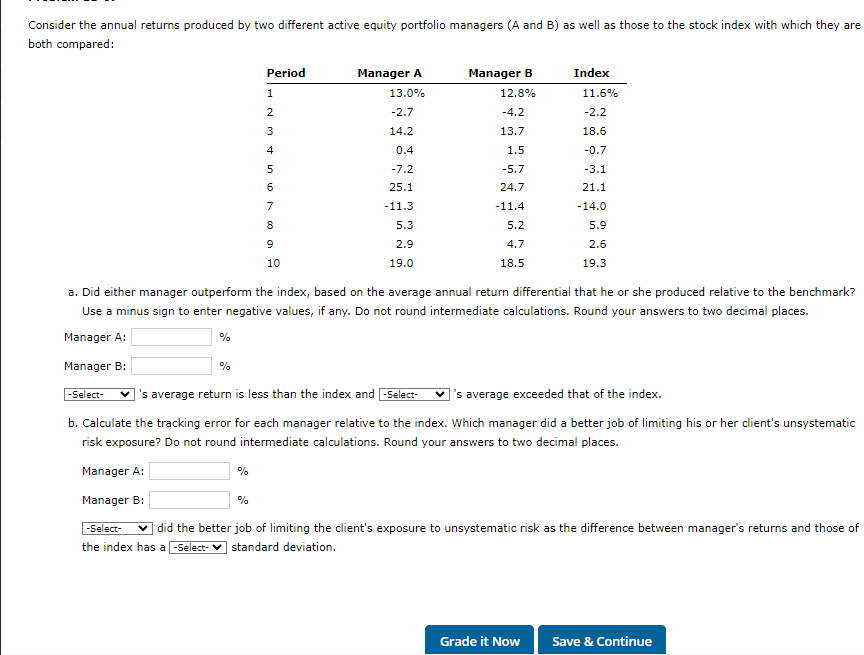

Consider the following trading and performance data for four different equity mutual funds: a. Calculate the portfolio turnover ratio for each fund. Do not round intermediate calculations. Round your answers to two decimal places. Fund W: % Fund X: % Fund Y : % Fund Z: % b. Which two funds are most likely to be actively managed and which two are most likely passive funds? are most likely passively managed portfolios; are most likely to be actively managed. c. Calculate the tax cost ratio for each fund. Do not round intermediate calculations. Round your answers to two decimal places. Fund W: % Fund X: % Fund Y: % Fund Z: % d. Which funds were the most and least tax efficient in the operations? were the most tax efficient and were the least tax efficient. As the chief investment officer for a money management firm specializing in taxable individual investors, you are trying to establish a strategic asset allocation for two different clients. You have established that Ms. A has a risk-tolerance factor of 9 , while Mr. B has a risk-tolerance factor of 24. The characteristics for four model portfolios follow: a. Calculate the expected utility of each prospective portfolio for each of the two clients. Do not round intermediate calculations. Round your answers to two decimal places. b. Which portfolio represents the optimal strategic allocation for Ms. A? Which portfolio is optimal for Mr. B? Portfolio represents the optimal strategic allocation for Ms. A. Portfolio is the optimal allocation for Mr. B. c. For Ms. A, what level of risk tolerance would leave her indifferent between having Portfolio 1 or Portfolio 2 as her strategic allocation? Round your answer to the nearest whole number. Consider the annual returns produced by two different active equity portfolio managers ( A and B ) as well as those to the stock index with which they are both compared: a. Did either manager outperform the index, based on the average annual return differential that he or she produced relative to the benchmark? Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers to two decimal places. Manager A: % Manager B: % 's average return is less than the index and 's average exceeded that of the index. b. Calculate the tracking error for each manager relative to the index. Which manager did a better job of limiting his or her client's unsystematic risk exposure? Do not round intermediate calculations. Round your answers to two decimal places. Manager A: % Manager B: % did the better job of limiting the client's exposure to unsystematic risk as the difference between manager's returns and those of the index has a standard deviation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts