Question: Consider the following two assets: Asset A's expected return is 3.5% and return standard deviation is 45% Asset B's expected return is 1.0% and

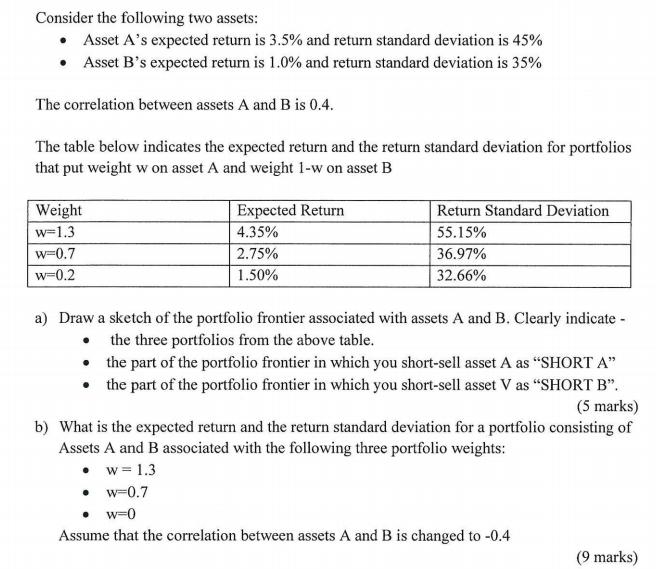

Consider the following two assets: Asset A's expected return is 3.5% and return standard deviation is 45% Asset B's expected return is 1.0% and return standard deviation is 35% The correlation between assets A and B is 0.4. The table below indicates the expected return and the return standard deviation for portfolios that put weight w on asset A and weight 1-w on asset B Weight w=1.3 w=0.7 w=0.2 Expected Return 4.35% 2.75% 1.50% Return Standard Deviation 55.15% 36.97% 32.66% a) Draw a sketch of the portfolio frontier associated with assets A and B. Clearly indicate - the three portfolios from the above table. the part of the portfolio frontier in which you short-sell asset A as "SHORT A" the part of the portfolio frontier in which you short-sell asset V as "SHORT B". (5 marks) b) What is the expected return and the return standard deviation for a portfolio consisting of Assets A and B associated with the following three portfolio weights: w=1.3 w=0.7 w=0 Assume that the correlation between assets A and B is changed to -0.4 (9 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts