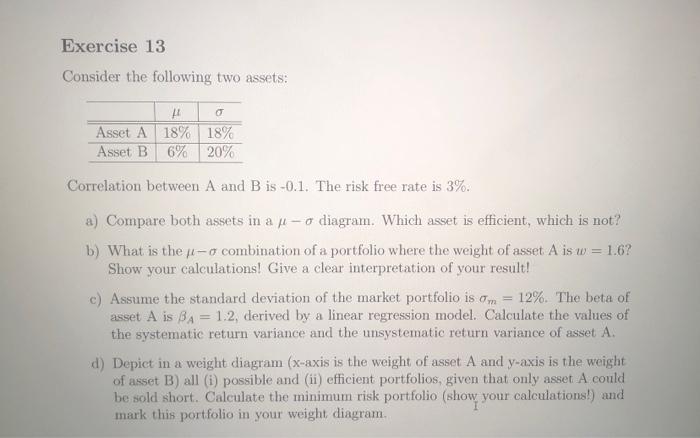

Question: Consider the following two assets: Correlation between A and B is 0.1. The risk free rate is 3%. a) Compare both assets in a diagram.

Consider the following two assets: Correlation between A and B is 0.1. The risk free rate is 3%. a) Compare both assets in a diagram. Which asset is efficient, which is not? b) What is the combination of a portfolio where the weight of asset A is w=1.6? Show your calculations! Give a clear interpretation of your result! c) Assume the standard deviation of the market portfolio is m=12%. The beta of asset A is A=1.2, derived by a linear regression model. Calculate the values of the systematic return variance and the unsystematic return variance of asset A. d) Depict in a weight diagram ( x-axis is the weight of asset A and y-axis is the weight of asset B) all (i) possible and (ii) efficient portfolios, given that only asset A could be sold short. Calculate the minimum risk portfolio (show your calculations!) and mark this portfolio in your weight diagram. Consider the following two assets: Correlation between A and B is 0.1. The risk free rate is 3%. a) Compare both assets in a diagram. Which asset is efficient, which is not? b) What is the combination of a portfolio where the weight of asset A is w=1.6? Show your calculations! Give a clear interpretation of your result! c) Assume the standard deviation of the market portfolio is m=12%. The beta of asset A is A=1.2, derived by a linear regression model. Calculate the values of the systematic return variance and the unsystematic return variance of asset A. d) Depict in a weight diagram ( x-axis is the weight of asset A and y-axis is the weight of asset B) all (i) possible and (ii) efficient portfolios, given that only asset A could be sold short. Calculate the minimum risk portfolio (show your calculations!) and mark this portfolio in your weight diagram

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts