Question: Consider the following two regression models: (1) Yi Bo + B Xi + Ui (2) Xi = Xi = ao + aYi + ei

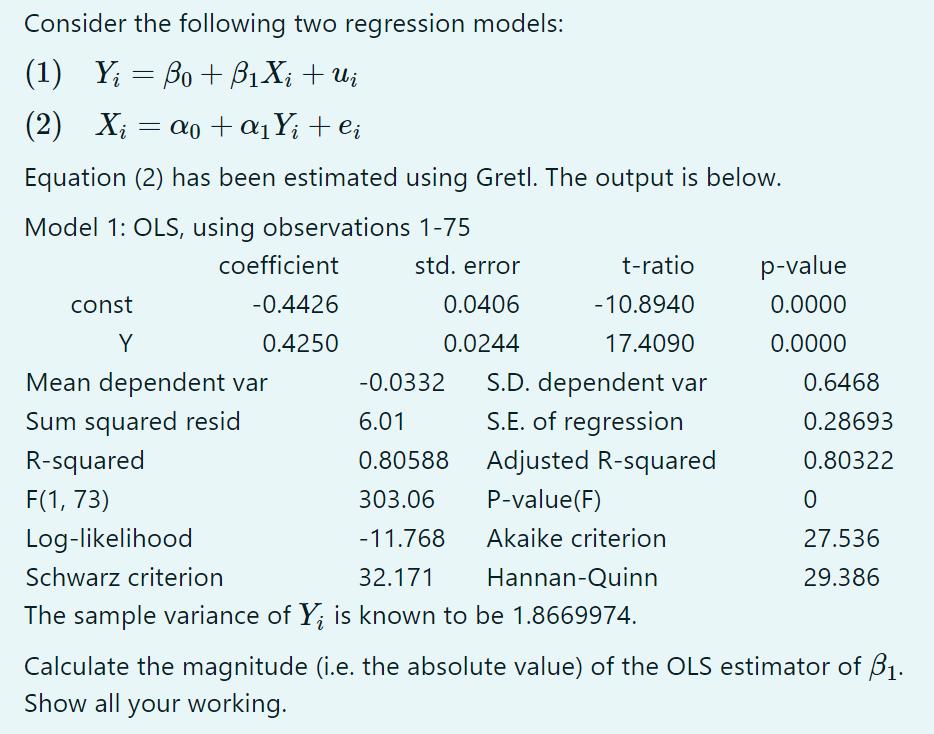

Consider the following two regression models: (1) Yi Bo + B Xi + Ui (2) Xi = Xi = ao + aYi + ei Equation (2) has been estimated using Gretl. The output is below. Model 1: OLS, using observations 1-75 const Y coefficient -0.4426 0.4250 Mean dependent var Sum squared resid R-squared F(1, 73) Log-likelihood std. error 0.0406 0.0244 t-ratio - 10.8940 17.4090 -0.0332 6.01 0.80588 303.06 -11.768 Schwarz criterion 32.171 Hannan-Quinn The sample variance of Y; is known to be 1.8669974. S.D. dependent var S.E. of regression Adjusted R-squared P-value (F) Akaike criterion p-value 0.0000 0.0000 0.6468 0.28693 0.80322 0 27.536 29.386 Calculate the magnitude (i.e. the absolute value) of the OLS estimator of B. Show all your working.

Step by Step Solution

3.36 Rating (152 Votes )

There are 3 Steps involved in it

Solution TO Let n conhelation Sx standand deiation of x Sy standard deviation o... View full answer

Get step-by-step solutions from verified subject matter experts