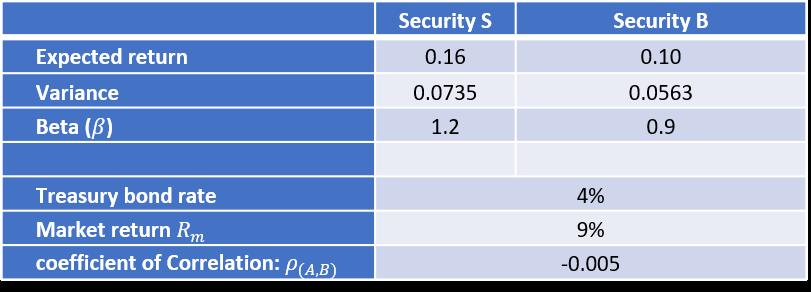

Consider the following two risky asset worlds: Answer the following questions: a. Explain why the risk of

Question:

Answer the following questions:

a. Explain why the risk of any portfolio composed of (S) and (B) is less than weighted average risk of the two securities.

b. Calculate the expected return and the variance of a portfolio composed of (60%: S, 40%: B).

c. If the minimum variance portfolio of the two securities is (43.41%: S, 56.59%: B), what is the expected return and the variance of this portfolio?

d. Explain Why the risk of any portfolio composed of S and B is greater than the risk of the portfolio in question.

e. Use the CAPM to evaluate the expected return of the two security (S).

f. Explain why the expected return calculated in question 5 equals to the market return if beta equals 1.

Expert Answer:

a The risk of a portfolio composed of securities S and B is less than the weighted average risk of the two securities because the correlation between ... View the full answer

Data Analysis and Decision Making

ISBN: 978-0538476126

4th edition

Authors: Christian Albright, Wayne Winston, Christopher Zappe