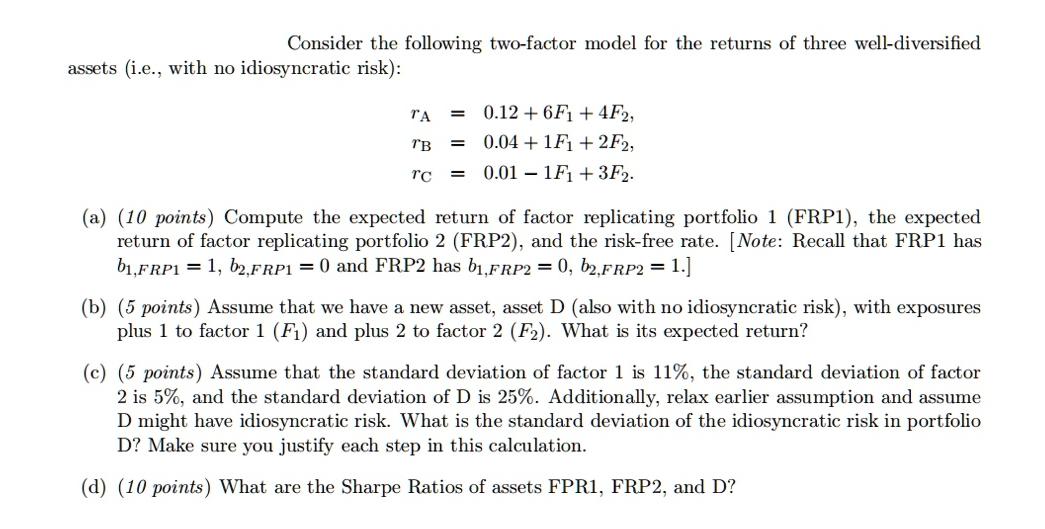

Consider the following two-factor model for the returns of three well-diversified assets (i.e., with no idiosyncratic...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a The expected return of factor replicating portfolio 1 FRPI is 6b1FRPI 4b2FRPI 61 40 6 Th... View the full answer

Related Book For

Understanding Basic Statistics

ISBN: 9781111827021

6th Edition

Authors: Charles Henry Brase, Corrinne Pellillo Brase

Posted Date: