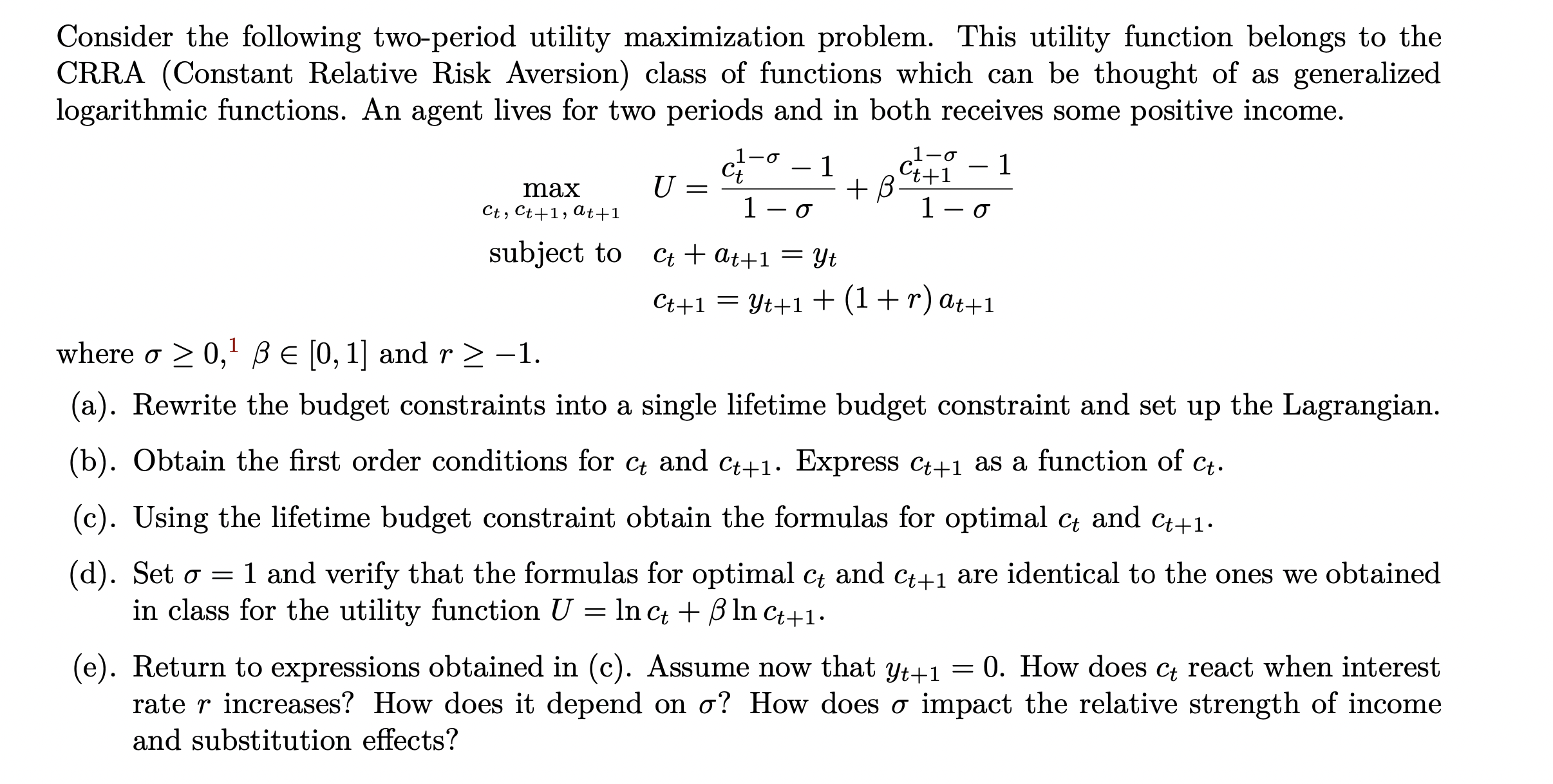

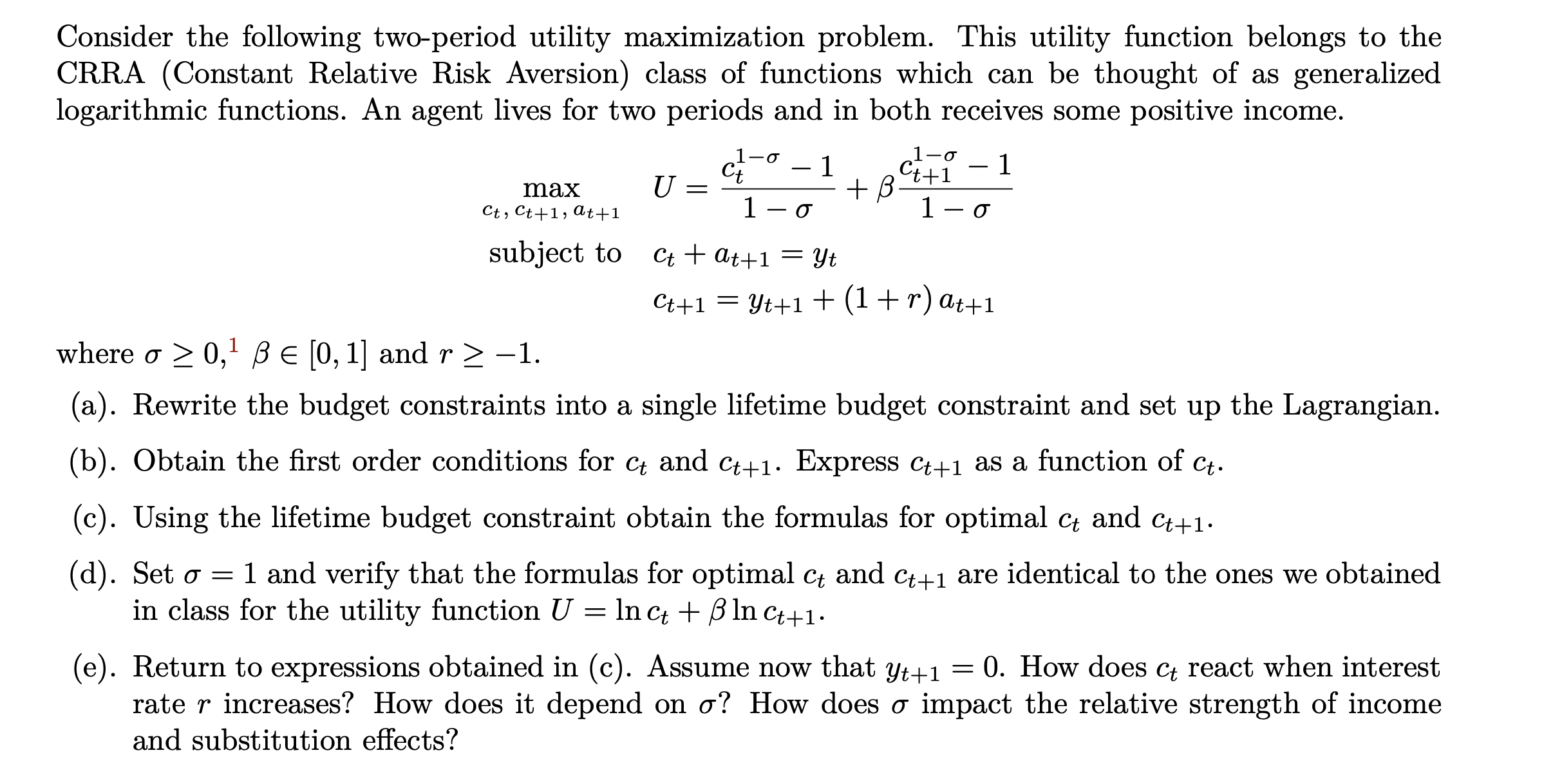

Question: Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought

Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought of as generalized logarithmic functions. An agent lives for two periods and in both receives some positive income. 10' _ 1 10' 1 C Gt 1 Ct,0t+1,at+1 1 0 10' subject to at + at+1 = in ct+1 = yt+1 + (1 + 7') at+1 where a 2 0,1 B 6 [0,1] and 7' Z 1. (a). Rewrite the budget constraints into a single lifetime budget constraint and set up the Lagrangian. (b). Obtain the rst order conditions for ct and ct+1. Express ct+1 as a function of ct. (c). Using the lifetime budget constraint obtain the formulas for optimal at and Ct+1. (d). Set a = 1 and verify that the formulas for optimal ct and ct+1 are identical to the ones we obtained in class for the utility function U = ln ct + B In Ct+1. (e). Return to expressions obtained in (c). Assume now that yt+1 = 0. How does ct react when interest rate 7" increases? How does it depend on a? How does a impact the relative strength of income and substitution effects

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts