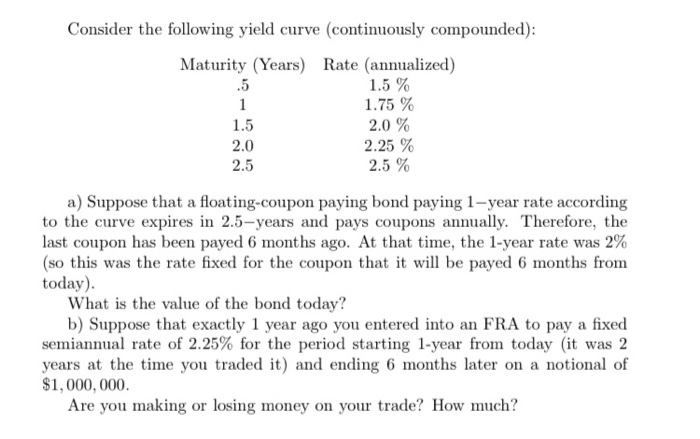

Question: Consider the following yield curve (continuously compounded): Maturity (Years) Rate (annualized) .5 1.5 % 1 1.75 % 2.0 % 2.0 2.25 % 2.5 2.5 %

Consider the following yield curve (continuously compounded): Maturity (Years) Rate (annualized) .5 1.5 % 1 1.75 % 2.0 % 2.0 2.25 % 2.5 2.5 % 1.5 a) Suppose that a floating-coupon paying bond paying 1-year rate according to the curve expires in 2.5-years and pays coupons annually. Therefore, the last coupon has been payed 6 months ago. At that time, the 1-year rate was 2% (so this was the rate fixed for the coupon that it will be payed 6 months from today). What is the value of the bond today? b) Suppose that exactly 1 year ago you entered into an FRA to pay a fixed semiannual rate of 2.25% for the period starting 1-year from today (it was 2 years at the time you traded it) and ending 6 months later on a notional of $1,000,000 Are you making or losing money on your trade? How much

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts