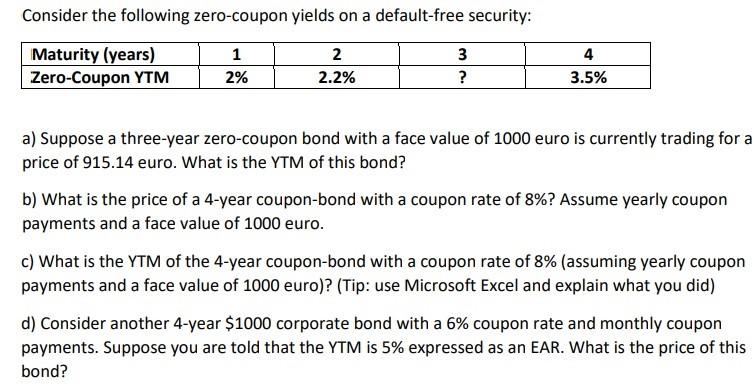

Question: Consider the following zero-coupon yields on a default-free security: Maturity (years) 1 2 3 Zero-Coupon YTM 2% 2.2% ? 4 3.5% a) Suppose a three-year

Consider the following zero-coupon yields on a default-free security: Maturity (years) 1 2 3 Zero-Coupon YTM 2% 2.2% ? 4 3.5% a) Suppose a three-year zero-coupon bond with a face value of 1000 euro is currently trading for a price of 915.14 euro. What is the YTM of this bond? b) What is the price of a 4-year coupon-bond with a coupon rate of 8%? Assume yearly coupon payments and a face value of 1000 euro. c) What is the YTM of the 4-year coupon-bond with a coupon rate of 8% (assuming yearly coupon payments and a face value of 1000 euro)? (Tip: use Microsoft Excel and explain what you did) d) Consider another 4-year $1000 corporate bond with a 6% coupon rate and monthly coupon payments. Suppose you are told that the YTM is 5% expressed as an EAR. What is the price of this bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts