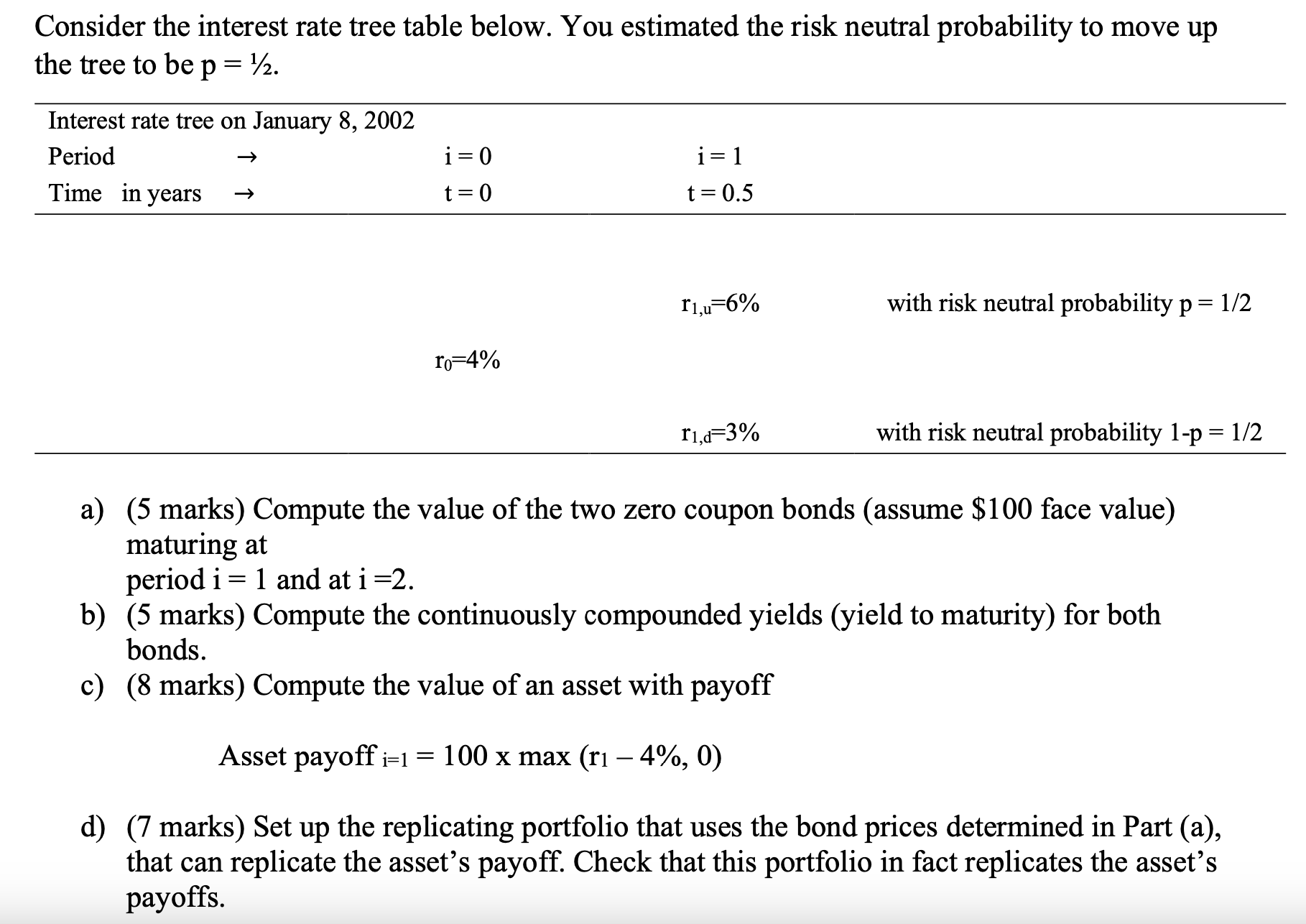

Question: Consider the interest rate tree table below. You estimated the risk neutral probability to move up the tree to be p = 1 2 .

Consider the interest rate tree table below. You estimated the risk neutral probability to move up

the tree to be

a marks Compute the value of the two zero coupon bonds assume $ face value

maturing at

period and at

b marks Compute the continuously compounded yields yield to maturity for both

bonds.

c marks Compute the value of an asset with payoff

Asset payoff max

d marks Set up the replicating portfolio that uses the bond prices determined in Part a

that can replicate the asset's payoff. Check that this portfolio in fact replicates the asset's

payoffs.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock