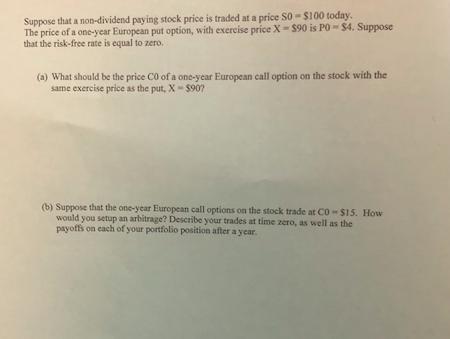

Suppose that a non-dividend paying stock price is traded at a price $0-$100 today. The price...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Probability and Statistics for Engineers and Scientists

ISBN: 978-0495107576

3rd edition

Authors: Anthony Hayter

Posted Date: