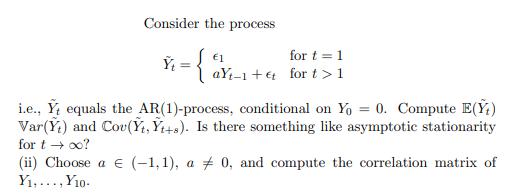

Consider the process Yt = {epsilon1 for t=1, aYt-1+epsilont for t>1. i.e., Y equals the AR(1)-process,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Introduction to Econometrics

ISBN: 978-0133595420

3rd edition

Authors: James H. Stock, Mark W. Watson

Posted Date: