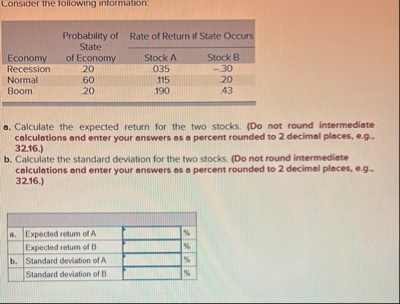

Question: Consider the rollowing intormation: table [ [ Econormy , Probability of State of Economy,Rate of Return if State Occurs ] , [ Stock A

Consider the rollowing intormation:

tableEconormyProbability of State of Economy,Rate of Return if State OccursStock AStock BRecessionNormalBoom

a Calculate the expected return for the two stocks. Do not round intermediate calculations and enter your answers as a percent rounded to decimal places, eg

b Calculate the standard deviation for the two stocks. Do not round intermediate calculations and enter your answers as o percent rounded to decimal places, eg

tableaExpected return of AExpected return of BbStandard deviation of AStandard deviation of B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock