Question: Consider the same model as in the previous problem . Gencarte 252 ( one year ) , 500 , 1000 , and 2500 separate time

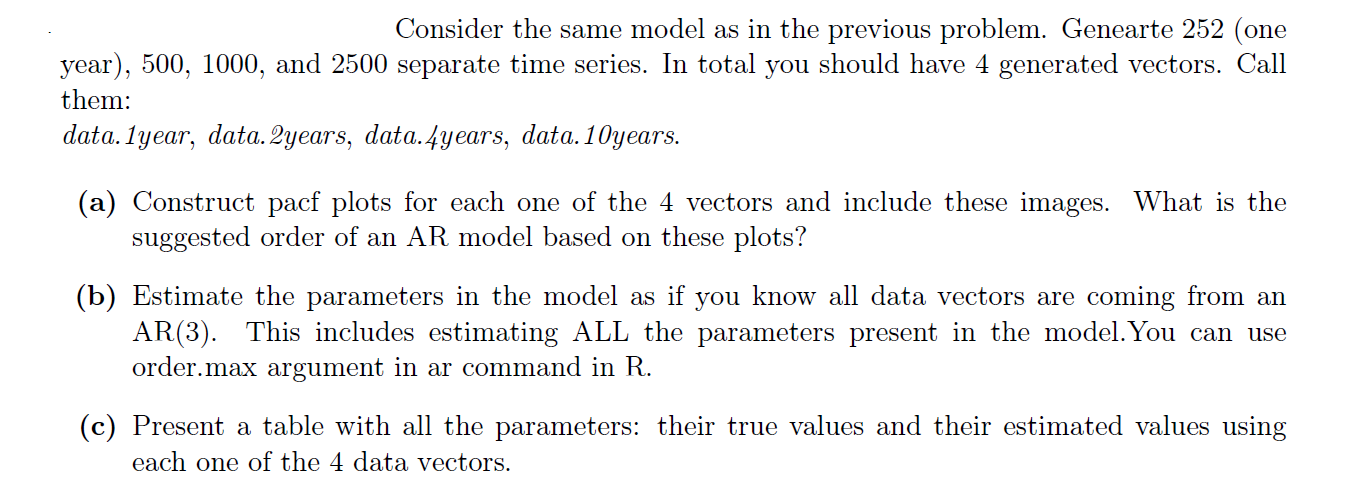

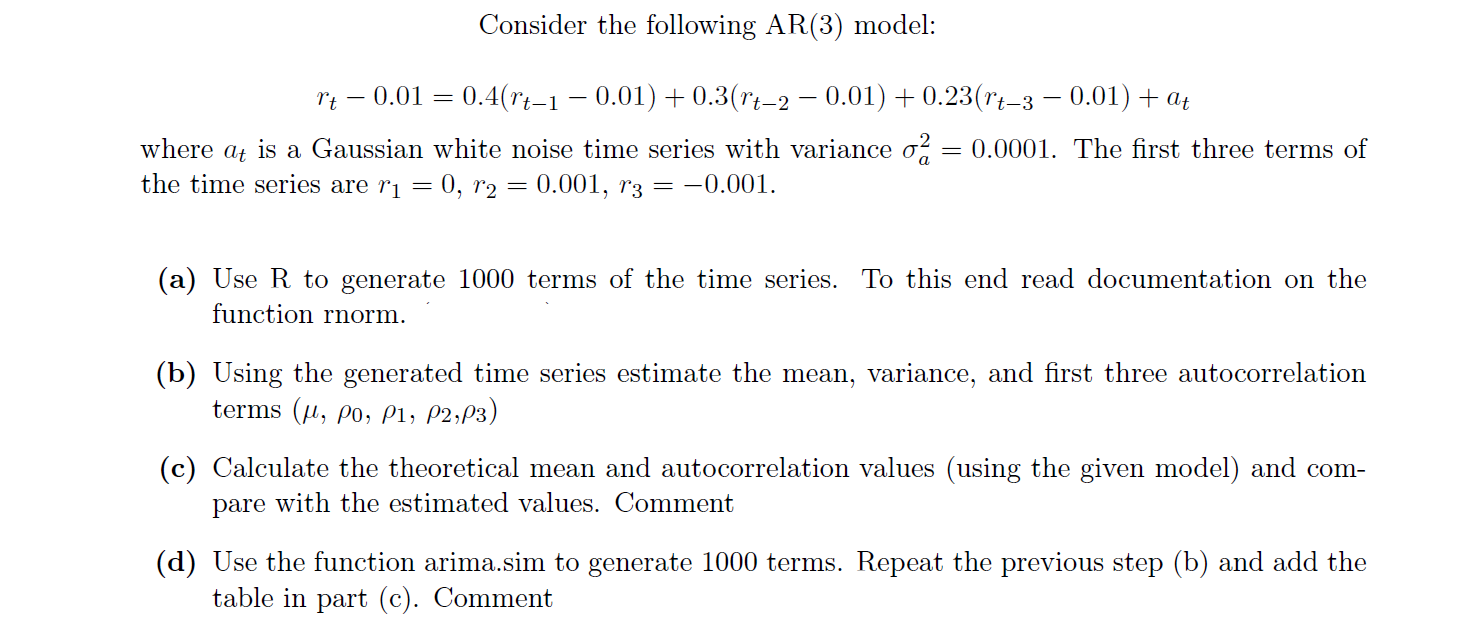

Consider the same model as in the previous problem . Gencarte 252 ( one year ) , 500 , 1000 , and 2500 separate time series . In total you should have 4 generated vectors . Call them ." data . I year , data . 2years , data . 4 years , data . 10 years . ( a ) Construct pact plots for each one of the 1 vectors and include these images . What is the suggested order of an AR model based on these plots ? ( b ) Estimate the parameters in the model as if you know all data vectors are coming from an AR ( 3 ) . This includes estimating ALL the parameters present in the model . You can use order . max argument in ar command in R . ( C ) Present a table with all the parameters : their true values and their estimated values using each one of the 1 data vectors .Consider the following AR(3) model: rt 7 0.01 = 0.4m;1 7 0.01) + 0.3(wH 7 0.01) + 0.23024, 7 0.01) + at where at is a Gaussian white noise time series with variance 0% = 0.0001. The rst three terms of the time series are r1 : 0, r2 : 0.001, \"r3 : 70.001. (a) Use R to generate 1000 terms of the time series. To this end read documentation on the function rnorm. ' i (b) Using the generated time series estimate the mean, variance, and rst three autocorrelation terms (N: no, pl, 92,93) (0) Calculate the theoretical mean and autocorrelation values (using the given model) and com pare with the estimated values. Comment ((1) Use the function arimasim to generate 1000 terms. Repeat the previous step (b) and add the table in part (0). Comment

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts