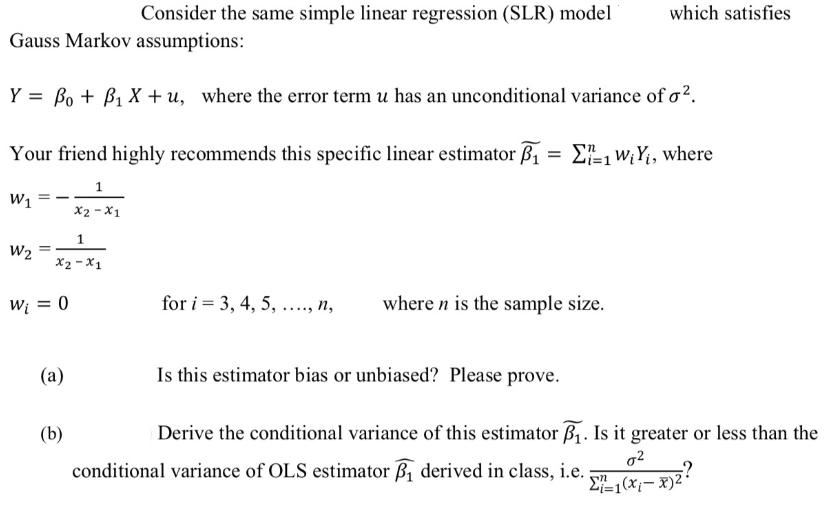

Question: Consider the same simple linear regression (SLR) model Gauss Markov assumptions: Y = Bo + B X + u, where the error term u

Consider the same simple linear regression (SLR) model Gauss Markov assumptions: Y = Bo + B X + u, where the error term u has an unconditional variance of o. Your friend highly recommends this specific linear estimator = 1 WY, where W1 W2 = 1 x2-xX1 W = 0 (a) 1 X2-X1 (b) for i= 3, 4, 5,...., n, where n is the sample size. which satisfies Is this estimator bias or unbiased? Please prove. Derive the conditional variance of this estimator P. Is it greater or less than the 0 conditional variance of OLS estimator P derived in class, i.e. ? =1(x; x)2

Step by Step Solution

3.38 Rating (160 Votes )

There are 3 Steps involved in it

a To determine whether the estimator 21WiYi is biased or unbiased we need to calculate its expectation E and compare it to the true population paramet... View full answer

Get step-by-step solutions from verified subject matter experts