Question: Consider the time series X t = 2 + 3 t + W t where W t are Gaussian white noises from N (0 ,

Consider the time series

Xt = 2 + 3t + Wt

where Wt are Gaussian white noises from N(0,1).

(1)Is Xt stationary? Why and why not.

(2)Is Yt = Xt ? Xt?1 stationary? Why and why not.

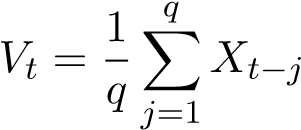

(3)Let

\f

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock