Question: Consider the yield curve with zero-coupon bonds at a face-value at 100: Maturity 1 2 3 Yield 4% 5% 6% 1. Calculate the expected

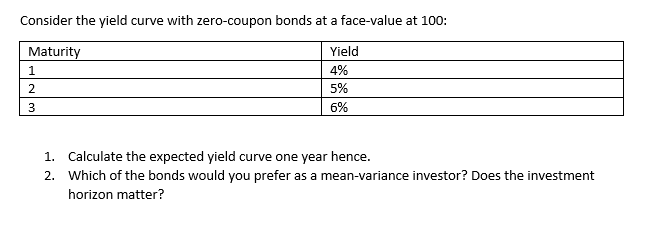

Consider the yield curve with zero-coupon bonds at a face-value at 100: Maturity 1 2 3 Yield 4% 5% 6% 1. Calculate the expected yield curve one year hence. 2. Which of the bonds would you prefer as a mean-variance investor? Does the investment horizon matter?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock