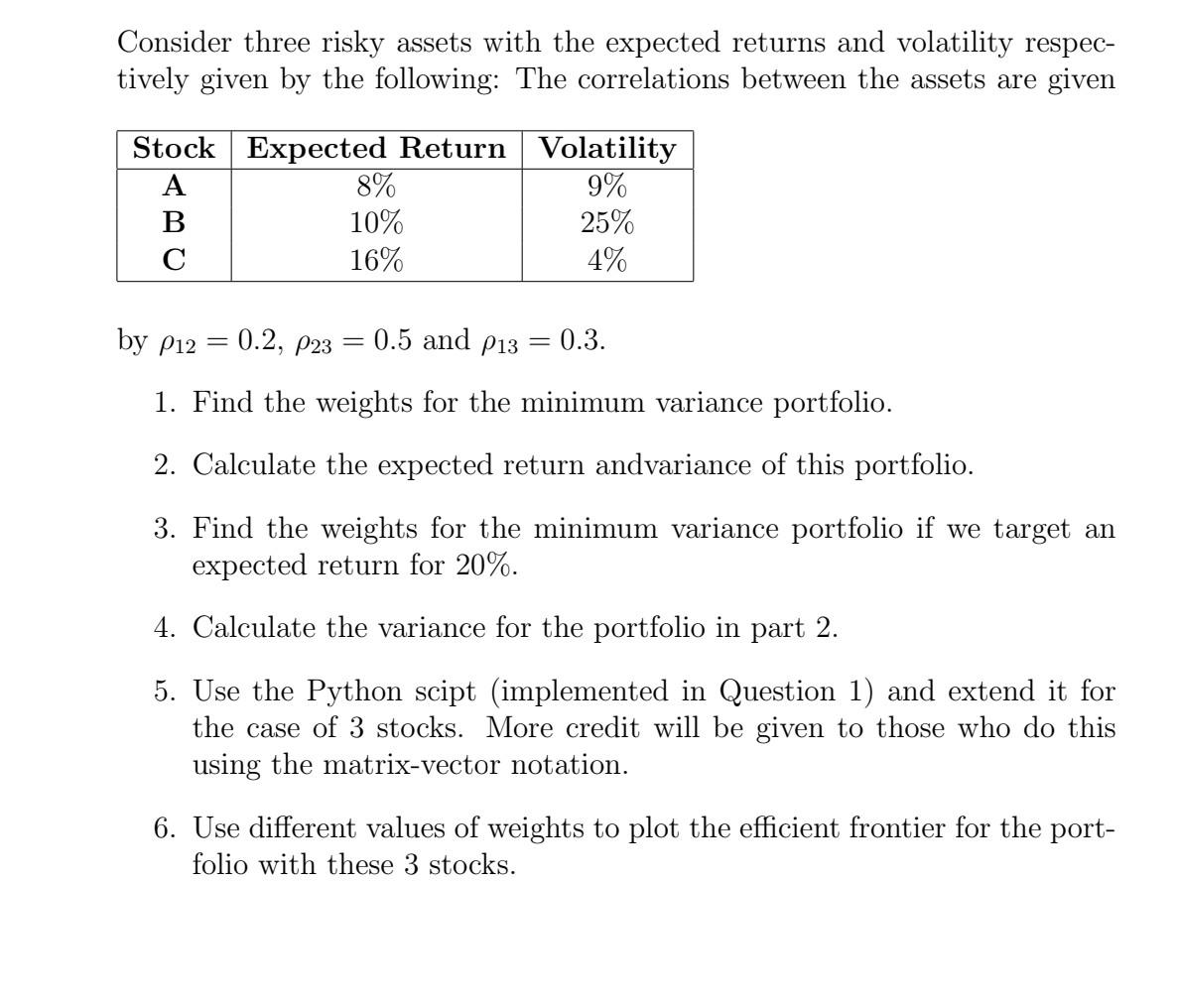

Question: Consider three risky assets with the expected returns and volatility respec- tively given by the following: The correlations between the assets are given Stock Expected

Consider three risky assets with the expected returns and volatility respec- tively given by the following: The correlations between the assets are given Stock Expected Return Volatility A 8% 9% B 10% 25% 16% 4% by P12 = 0.2, P23 0.5 and p13 = 0.3. 1. Find the weights for the minimum variance portfolio. 2. Calculate the expected return andvariance of this portfolio. 3. Find the weights for the minimum variance portfolio if we target an expected return for 20%. 4. Calculate the variance for the portfolio in part 2. 5. Use the Python scipt (implemented in Question 1) and extend it for the case of 3 stocks. More credit will be given to those who do this using the matrix-vector notation. 6. Use different values of weights to plot the efficient frontier for the port- folio with these 3 stocks. Consider three risky assets with the expected returns and volatility respec- tively given by the following: The correlations between the assets are given Stock Expected Return Volatility A 8% 9% B 10% 25% 16% 4% by P12 = 0.2, P23 0.5 and p13 = 0.3. 1. Find the weights for the minimum variance portfolio. 2. Calculate the expected return andvariance of this portfolio. 3. Find the weights for the minimum variance portfolio if we target an expected return for 20%. 4. Calculate the variance for the portfolio in part 2. 5. Use the Python scipt (implemented in Question 1) and extend it for the case of 3 stocks. More credit will be given to those who do this using the matrix-vector notation. 6. Use different values of weights to plot the efficient frontier for the port- folio with these 3 stocks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts