Question: Consider two asset classes: Stocks and Bonds. You estimate the following parameters for these two asset class funds. correlation matrix b Stocks and Bonds E(1)

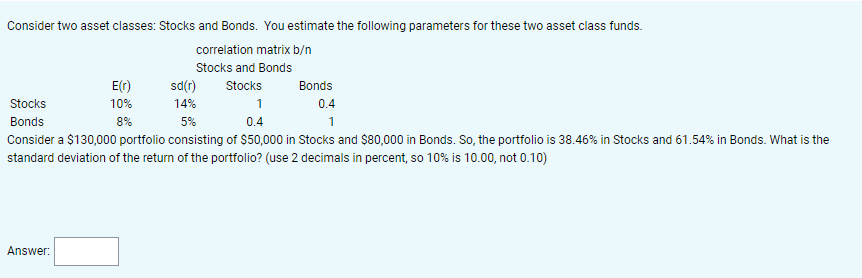

Consider two asset classes: Stocks and Bonds. You estimate the following parameters for these two asset class funds. correlation matrix b Stocks and Bonds E(1) sd(r) Stocks Bonds Stocks 10% 14% 1 0.4 Bonds 8% 5% 0.4 1 Consider a $130,000 portfolio consisting of $50,000 in Stocks and $80,000 in Bonds. So, the portfolio is 38.46% in Stocks and 61.54% in Bonds. What is the standard deviation of the return of the portfolio? (use 2 decimals in percent, so 10% is 10.00, not 0.10)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock