Question: Consider two bonds Bond A and Bond B. Bond A has a maturity of 1.5 years and pays coupons semi-annually at the rate of 10%

Consider two bonds Bond A and Bond B. Bond A has a maturity of 1.5 years and pays coupons semi-annually at the rate of 10% per year. Its yield to maturity is 3.9050% p.a., semi- annual compounding. Bond B has a maturity of 3 years and pays coupons semi-annually at the rate of 7% per year. Its yield to maturity is 4.4805% p.a., semi-annual compounding. What are the spot interest rates for the terms of 1 year and 2 years?

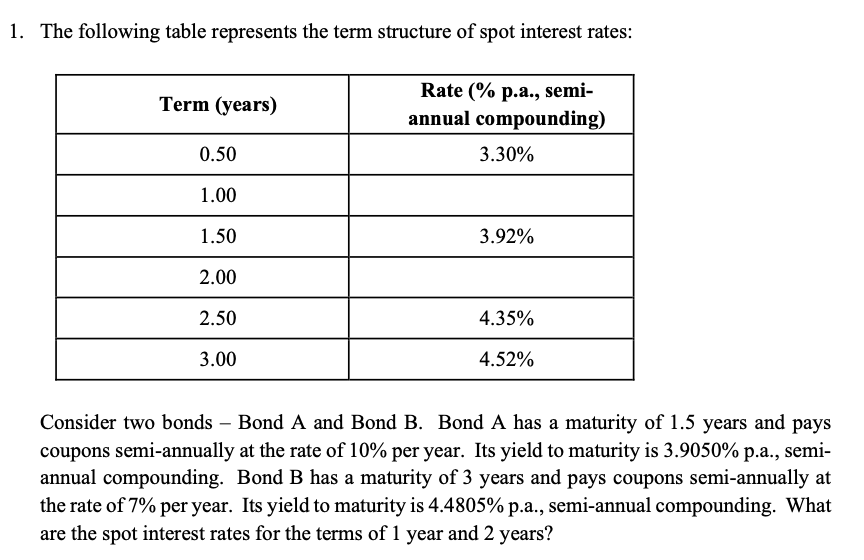

The following table represents the term structure of spot interest rates: Consider two bonds - Bond A and Bond B. Bond A has a maturity of 1.5 years and pays coupons semi-annually at the rate of 10% per year. Its yield to maturity is 3.9050% p.a., semiannual compounding. Bond B has a maturity of 3 years and pays coupons semi-annually at the rate of 7% per year. Its yield to maturity is 4.4805% p.a., semi-annual compounding. What are the spot interest rates for the terms of 1 year and 2 years

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts