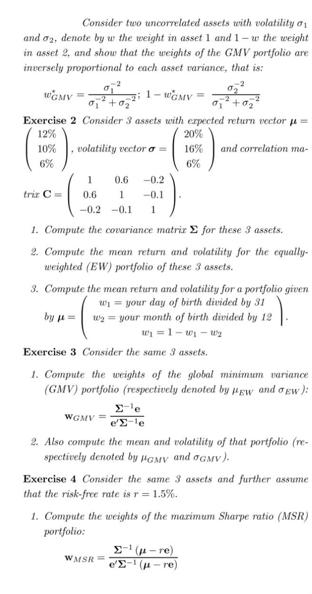

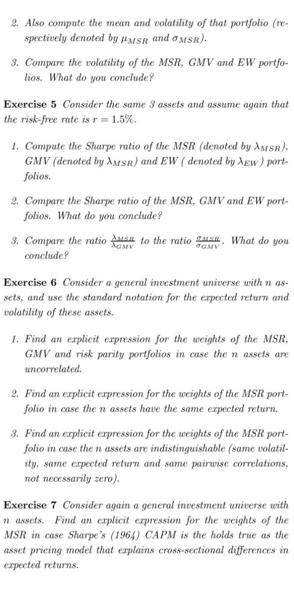

Consider two uncorrelated assets with volatility a and 02, denote by w the weight in asset...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Here are the solutions to the exercises Exercise 2 1 Covariance matrix for the 3 assets 004 008 012 ... View the full answer

Related Book For

Introduction to Algorithms

ISBN: 978-0262033848

3rd edition

Authors: Thomas H. Cormen, Charles E. Leiserson, Ronald L. Rivest

Posted Date: