Question: CONSTRUCTING A REPLICATING PORTFOLIO Suppose a 2-year fixed income security exists with $100 face value and a 10% coupon rate. The coupons are paid on

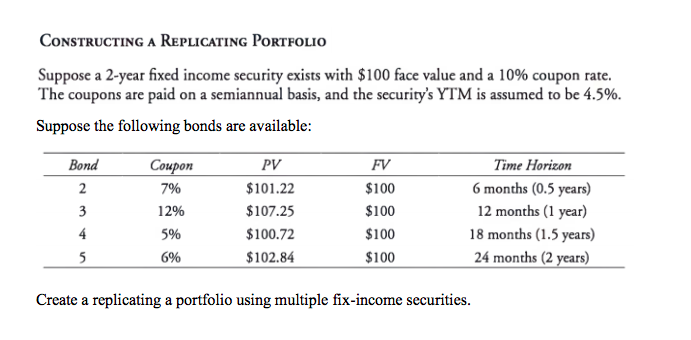

CONSTRUCTING A REPLICATING PORTFOLIO Suppose a 2-year fixed income security exists with $100 face value and a 10% coupon rate. The coupons are paid on a semiannual basis, and the security's YTM is assumed to be 4.5%. Suppose the following bonds are available PV $101.22 $107.25 $100.72 $102.84 ime Horizon 6 months (0.5 years) 12 months (1 year) 18 months (1.5 years) 24 months (2 years) Bond Cou FV $100 $100 $100 $100 7% 12% 596 6% Create a replicating a portfolio using multiple fix-income securities CONSTRUCTING A REPLICATING PORTFOLIO Suppose a 2-year fixed income security exists with $100 face value and a 10% coupon rate. The coupons are paid on a semiannual basis, and the security's YTM is assumed to be 4.5%. Suppose the following bonds are available PV $101.22 $107.25 $100.72 $102.84 ime Horizon 6 months (0.5 years) 12 months (1 year) 18 months (1.5 years) 24 months (2 years) Bond Cou FV $100 $100 $100 $100 7% 12% 596 6% Create a replicating a portfolio using multiple fix-income securities

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts