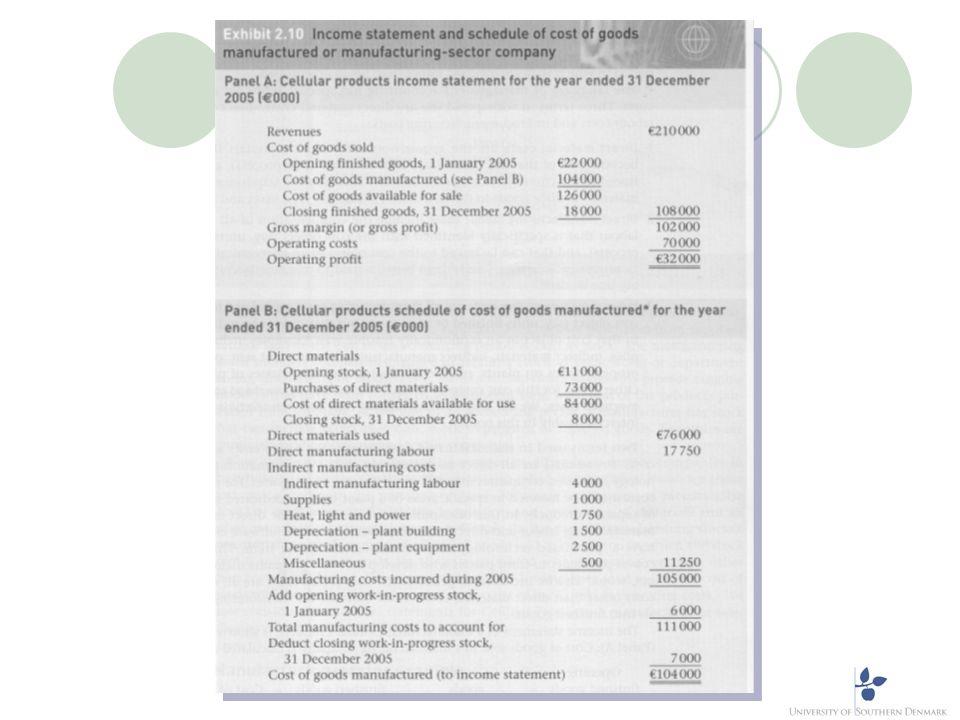

Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A:...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK Exhibit 2.10 Income statement and schedule of cost of goods manufactured or manufacturing-sector company Panel A: Cellular products income statement for the year ended 31 December 2005 (€000) Revenues €210000 Cost of goods sold Opening finished goods, 1 January 2005 Cost of goods manufactured (see Panel B) Cost of goods available for sale Closing finished goods, 31 December 2005 Gross margin (or gross profit) Operating costs Operating profit €22000 104000 126000 18000 108000 102000 70000 €32000 Panel B: Cellular products schedule of cost of goods manufactured for the year ended 31 December 2005 (€000) Direct materials Opening stock, 1 January 2005 Purchases of direct materials Cost of direct materials available for use €11000 73000 84 000 Closing stock, 31 December 2005 Direct materials used 8000 €76000 17750 Direct manufacturing labour Indirect manufacturing costs Indirect manufacturing labour Supplies Heat, light and power Depreciation- plant building Depreciation - plant equipment Miscellaneous Manufacturing costs incurred during 2005 Add opening work-in-progress stock, 1 January 2005 Total manufacturing costs to account for Deduct closing work-in-progress stock, 31 December 200S Cost of goods manufactured (to income statement) 4000 1000 1750 1 500 2500 500 11250 105 000 6000 111000 7000 €104000 UNIVERSITY OF SOUTHERN DENMARK

Expert Answer:

Answer rating: 100% (QA)

Sol Step 1Information Given Beginning Inventory 22000 Cost goods of Manufacture... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Inventory and cost of goods sold information for Lafleche Inc. is provided below: Required: a. Calculate the inventory turnover ratio and average number of days in inventory under the two cost...

-

Inventory and cost of goods sold figures prepared under the LIFO cost flow assumption versus the FIFO cost flow assumption can differ dramatically. Required: a. Would an analyst consider ending...

-

Inventory turnover is calculated as cost of goods sold divided by ending inventory . 1. True 2. False

-

Question 5 [ 4 points ] In the table shown below is accounting equation information as it applies to Second Time Around Clothing. Calculate the missing amounts assuming that a . Assets decreased by $...

-

Solve Problem 16.20 but assume that the downtime (Td = 6.0 min) follows the geometric repair distribution. Problem 16.20 In Problem 16.18, if the capacity of the proposed storage buffer is to be 20...

-

What is a shell company and how is it formed?

-

A circuit board with a dense distribution of integrated circuits (ICs) and dimensions of \(20 \mathrm{~mm} \times 20 \mathrm{~mm}\) on a side is cooled by the parallel flow of atmospheric air with a...

-

Sierra Company incurs the following costs to produce and sell a single product. During the last year, 25,000 units were produced and 22,000 units were sold. The Finished Goods inventory account at...

-

Cullumber is a Canadian company that conducts many transactions in $US. Because the price of $US fluctuates daily, Cullumber often enters into futures contracts as a way to manage risk. On September...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

Federico Buenrostro was the CEO of the California Public Employees' Retirement System (CaIPERS) from 2002 to 2008; Alfred Villalobos was a CaIPERS board member from 1993 to 1995. Buenrostro created...

-

Aqua gym ltd is boutique gym chai that operates in Sydney area. Aqua gym offers an annual membership at a price of $12,000. After costumers pays an upfront cash payment of the annual membership fee...

-

Smallville Bank has the following balance sheet, rates earned on its assets, and rates paid on its liabilities. Balance Sheet (in thousands) Assets Cash and due from banks Rate Earned (%) $ 6,000 0...

-

Because you determine an estimate of the uncertainty, it should not be stated with too much precision. Experimental uncertainties should almost always be rounded to one significant figure. The main...

-

observational and epidemiological studies, some physicians have long believed that HIV-infected individuals who receive antiretroviral treatments (ART) pose a lower risk of transmitting the virus to...

-

(A) The following chargeable persons have Malaysian sources of income and remittances of foreign sources of income for the basis year of 2020: Chargeable persons Mr Yeo (Resident) Ms Janet...

-

Common stock value-Variable growth Lawrence Industries' most recent annual dividend was $1.39 per share (Do $1.39), and the firm's required return is 10%. Find the market value of Lawrence's shares...

-

Time Travel Publishing was recently organized. The company issued common stock to an attorney who provided legal services worth $25,000 to help organize the corporation. Time Travel also issued...

-

Why might users prefer the direct method of preparing a statement of cash flows to the indirect method? Which method is more commonly used? Why?

-

How is the book value of a depreciable asset computed? How does a depreciable assets book value change from one accounting period to the next? Discuss the difference between the terms book value and...

-

CALAir is a small charter airline company that operates between San Francisco and Los Angeles. On January 2, 2009, CALAir purchased a jet costing $2,600,000 with an estimated salvage value of...

-

The hangers support the joist in such a way that the four nails on each hanger can be assumed to support an equal portion of the load. If the joist is subjected to the loading shown, determine the...

-

The 60 mm x 60 mm oak post is supported on the pine block. If the allowable bearing stresses for these materials are oak = 43 MPa and pine 25 MPa, determine the greatest load P that can be...

-

The hangers support the joist in such a way that the four nails on each hanger can be assumed to support an equal portion of the load. Determine the smallest diameter of the nails at A and B to the...

Study smarter with the SolutionInn App