Question: could u please help me to solve? Thanks 2. Consider the following data (interest rate is per period):- S = 100; K= 75; R =

could u please help me to solve? Thanks

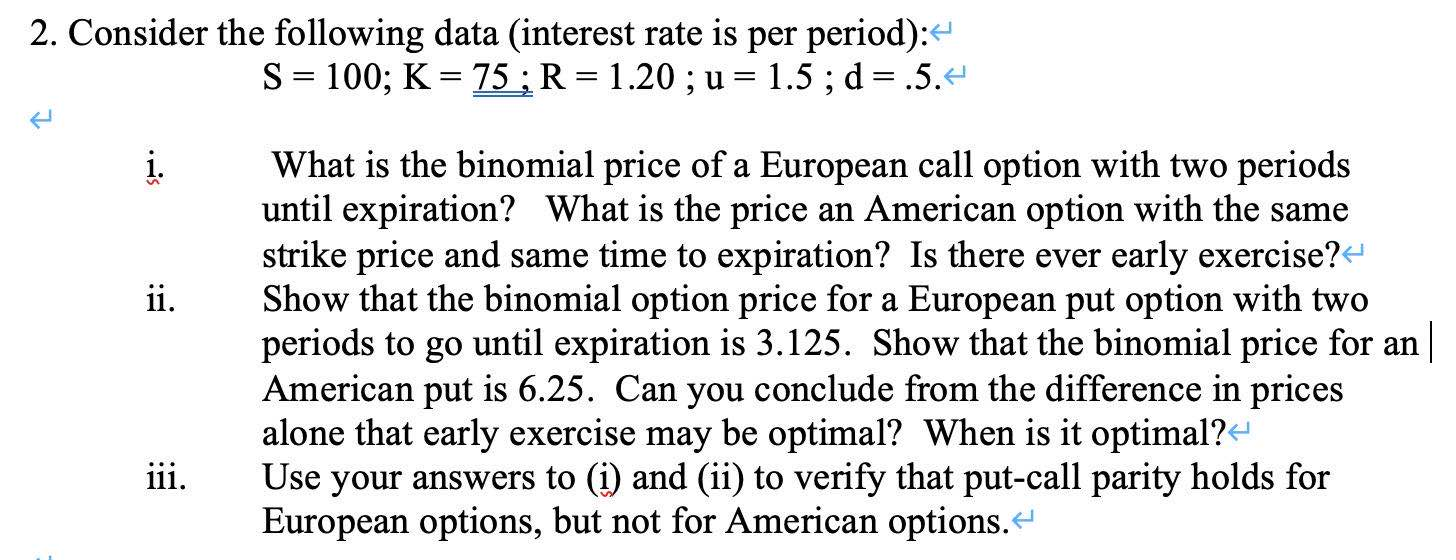

2. Consider the following data (interest rate is per period):- S = 100; K= 75; R = 1.20; u= 1.5; d= .5.4 7 i. ii. What is the binomial price of a European call option with two periods until expiration? What is the price an American option with the same strike price and same time to expiration? Is there ever early exercise? Show that the binomial option price for a European put option with two periods to go until expiration is 3.125. Show that the binomial price for an | American put is 6.25. Can you conclude from the difference in prices alone that early exercise may be optimal? When is it optimal?4 Use your answers to (i) and (ii) to verify that put-call parity holds for European options, but not for American options

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts