Question: Could you make the error corrections both assuming the books are open and then they are closed and the amounts are in Retained earnings. Ty

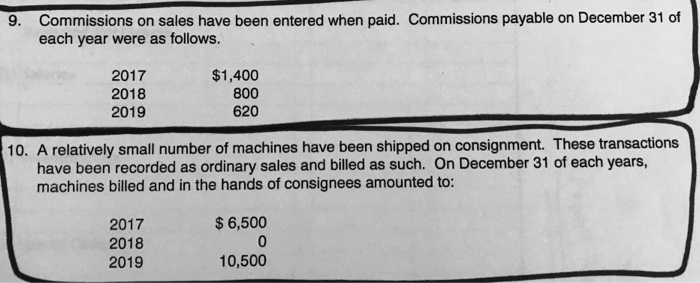

December 2019 Overstated $ 6,000 Jackson, Inc. purchased $4,500 of supplies on December 19, 2019 recording a debit to Supplies and credit to Accounts Payable. The bill was paid on December 26, 2019, but not recorded until January 2, 2020. In 2019. the company sold for $3,500 equipment that had a book value of $2,000 and originally At December 31, 2019 Jackson, Inc. decided to change the depreciation method on its machinery from double-declining-balance to straight-line. The Machinery had an original cost of $100,000 when purchased on July 1, 2017 it has a 10-year useful life and no salvage value. Depreciation expense recorded prior to 2019 under the double-declining-balance method was $28,000. Jackson, Inc. has already recorded 2019 depreciation expense of $14,400 using the double-declining balance 9. Commissions on sales have been entered when paid. Commissions payable on December 31 of each year were as follows. 2017 2018 2019 $1,400 800 620 10. A relatively small number of machines have been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such. On December 31 of each years, machines billed and in the hands of consignees amounted to: 2017 $6,500 2018 2019 10,500

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts