Question: Could you please solve this two questions? The yield on a two year T-no tes is 4% and the return on a one year T-bill

Could you please solve this two questions?

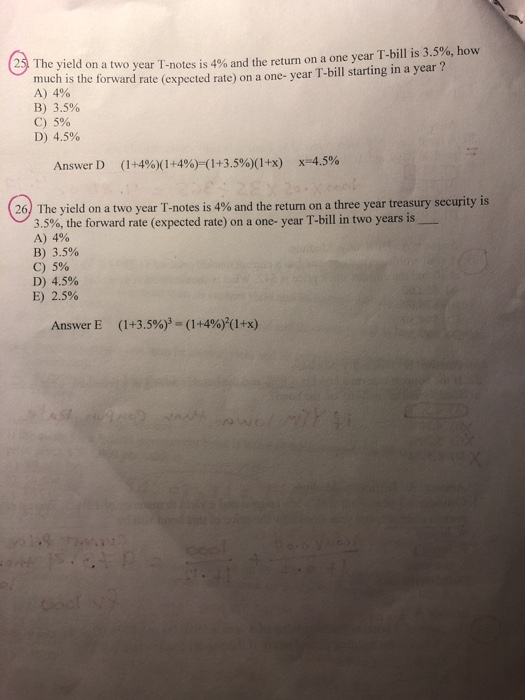

The yield on a two year T-no tes is 4% and the return on a one year T-bill is 3.5%, how ch is the forward rate (expected rate) on a one- year T-bill starting in a year ? A) 4% B) 3.5% C) 5% D) 4.5% Answer D (14%)(1+4%)-(1+3.5%)(1+x) x-4.5% 26) The yield on a two year T-notes is 4% and the return on a three year treasury security is 3.5%, the forward rate (expected rate) on a one-year T-bill in two years is A) 4% B) 3.5% C) 5% D) 4.5% E) 2.5% Answer E (1+3.5%)-(1+4%)2(1+x)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock