Question: could you show how to do this in excel Solve using Microsoft Excel Upload your excel file in Black Board Econ. Prob. T-Bill Ultra Inc

could you show how to do this in excel

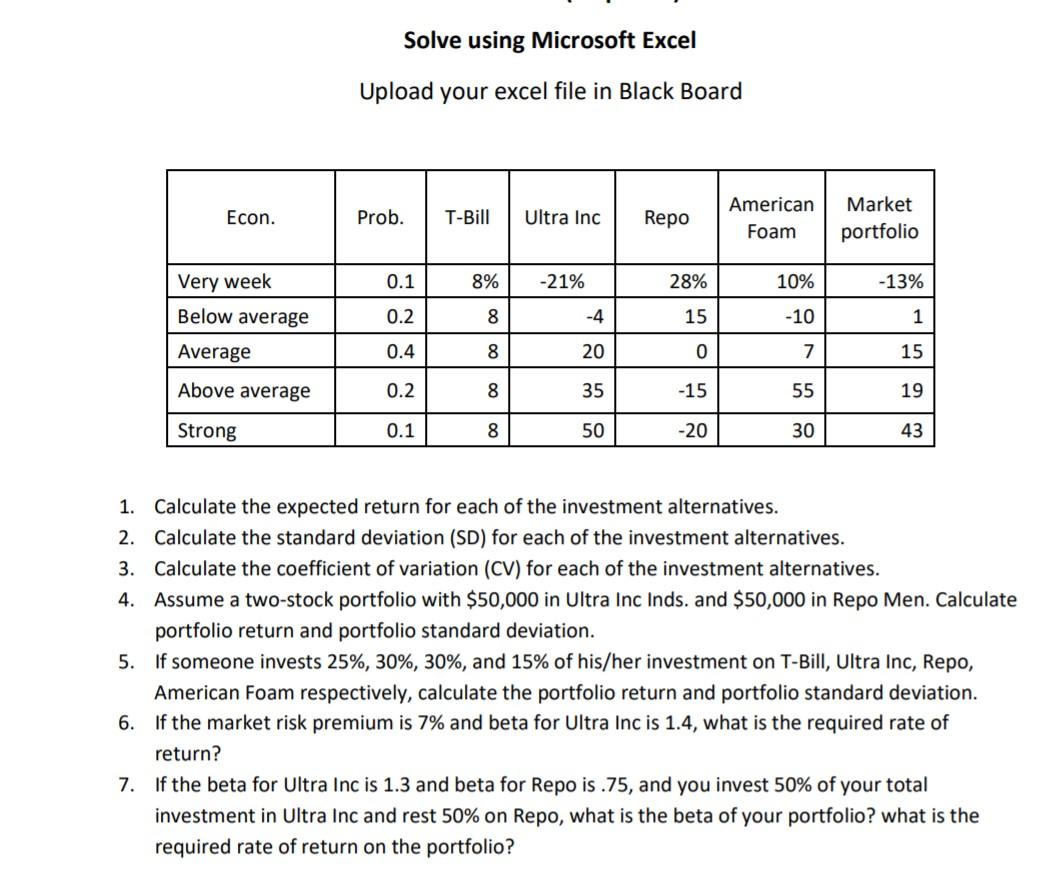

Solve using Microsoft Excel Upload your excel file in Black Board Econ. Prob. T-Bill Ultra Inc Repo American Foam Market portfolio Very week 0.1 8% -21% 28% 10% -13% Below average 0.2 8 -4 15 -10 1 Average 0.4 8 20 0 7 15 Above average 0.2 8 35 -15 55 19 Strong 0.1 8 50 -20 30 43 1. Calculate the expected return for each of the investment alternatives. 2. Calculate the standard deviation (SD) for each of the investment alternatives. 3. Calculate the coefficient of variation (CV) for each of the investment alternatives. 4. Assume a two-stock portfolio with $50,000 in Ultra Inc Inds. and $50,000 in Repo Men. Calculate portfolio return and portfolio standard deviation. 5. If someone invests 25%, 30%, 30%, and 15% of his/her investment on T-Bill, Ultra Inc, Repo, American Foam respectively, calculate the portfolio return and portfolio standard deviation. 6. If the market risk premium is 7% and beta for Ultra Inc is 1.4, what is the required rate of return? 7. If the beta for Ultra Inc is 1.3 and beta for Repo is .75, and you invest 50% of your total investment in Ultra Inc and rest 50% on Repo, what is the beta of your portfolio? what is the required rate of return on the portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts