Question: Crane Co. uses a perpetual inventory system and both an accounts receivable and an accounts payable subsidiary ledger. Balances related to both the general

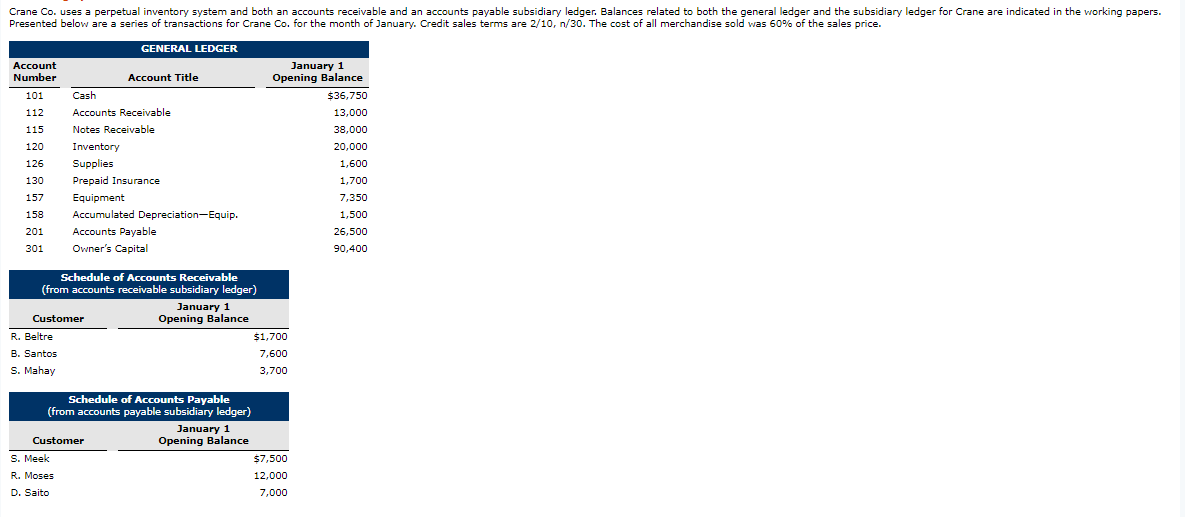

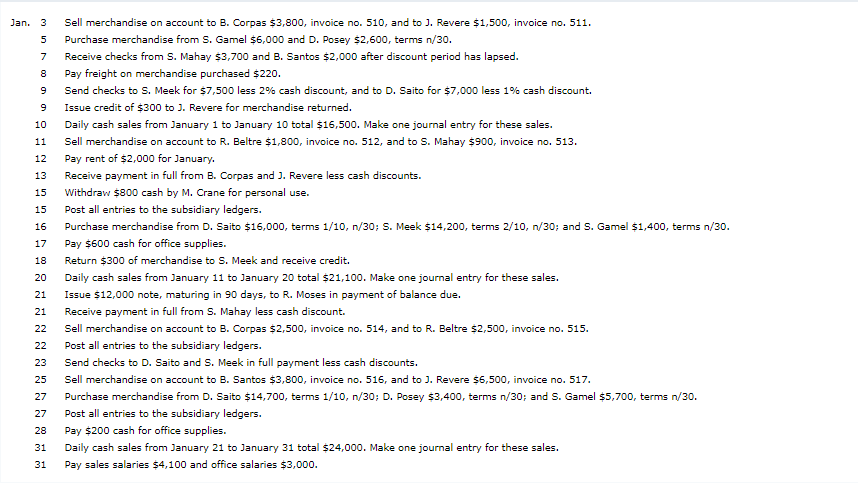

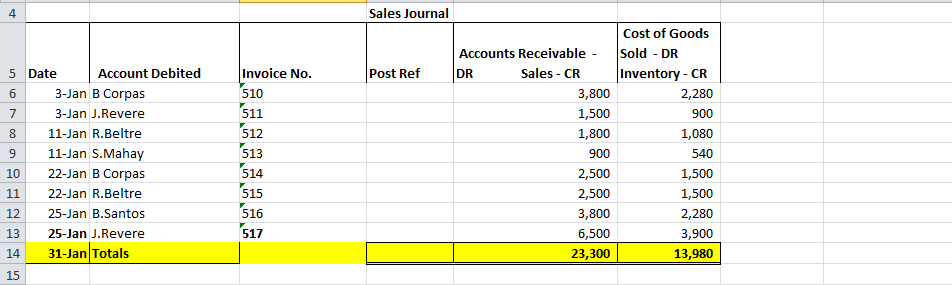

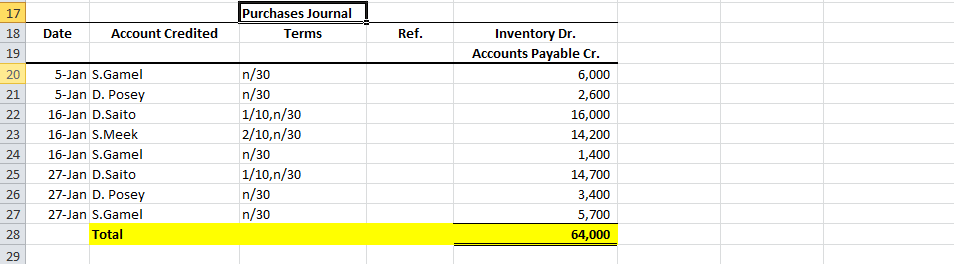

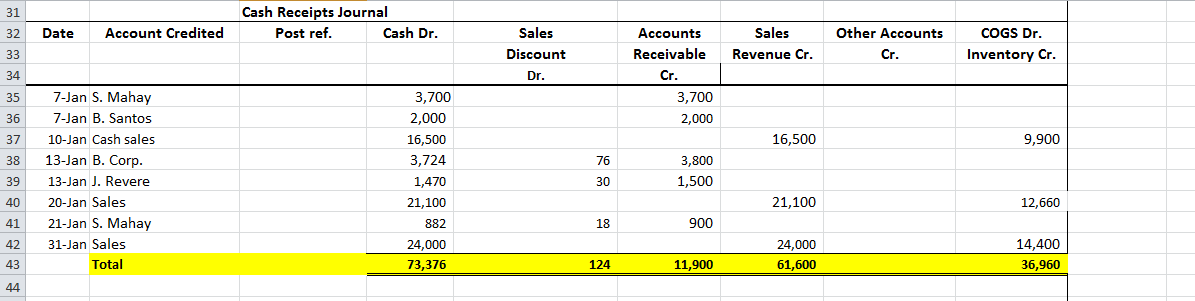

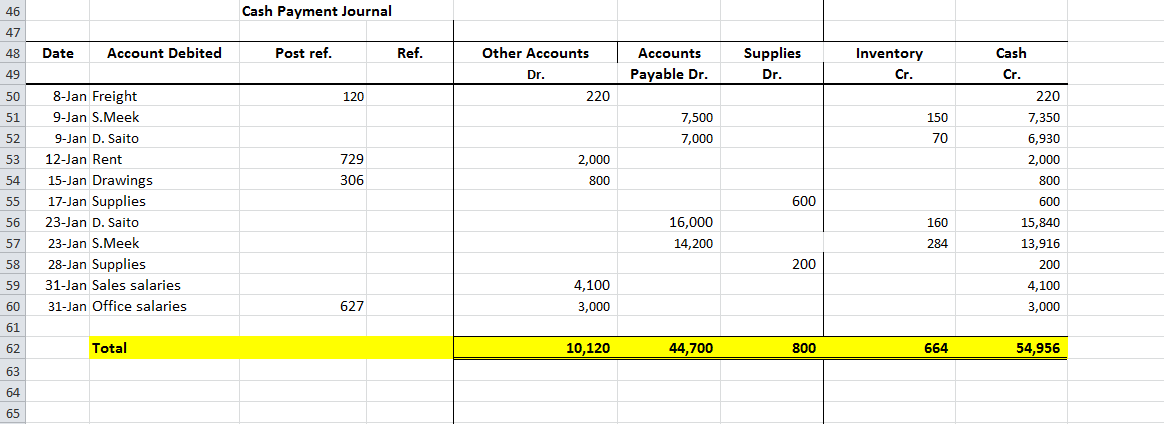

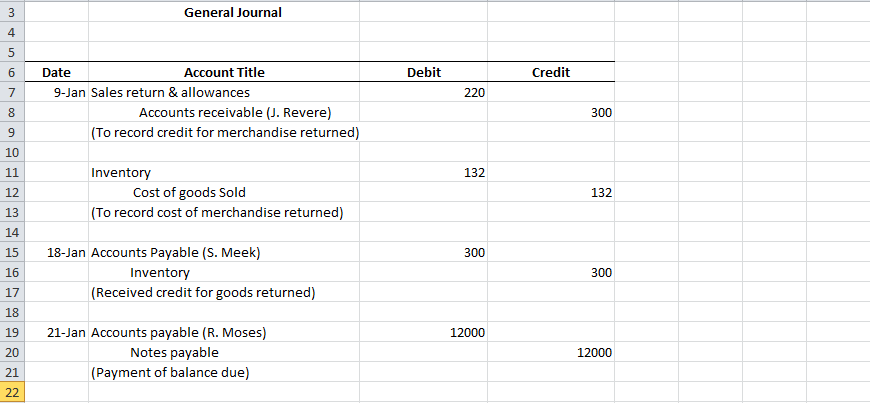

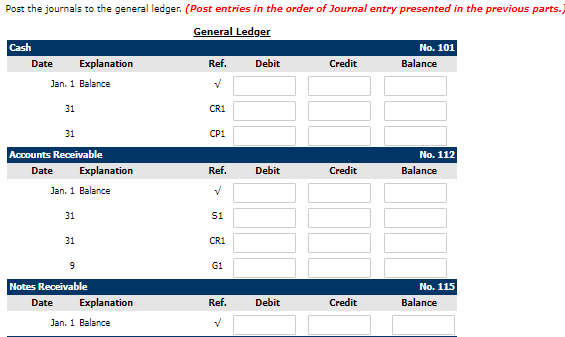

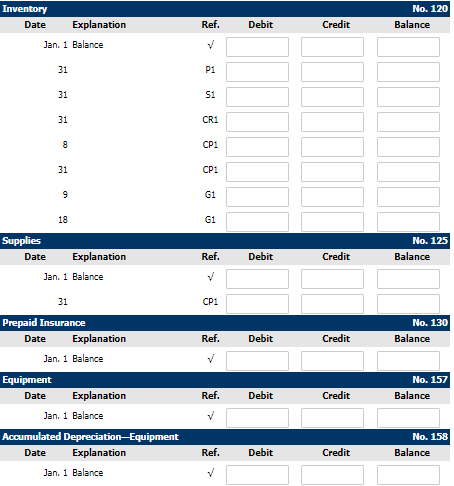

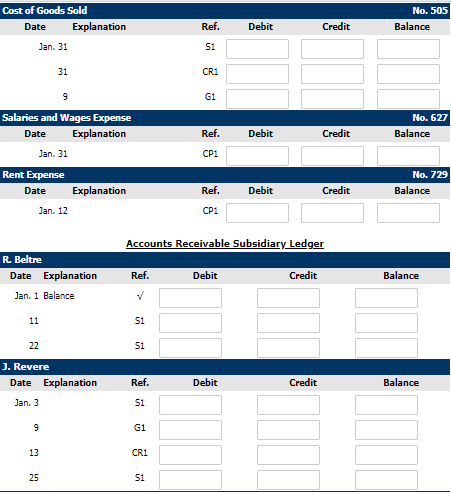

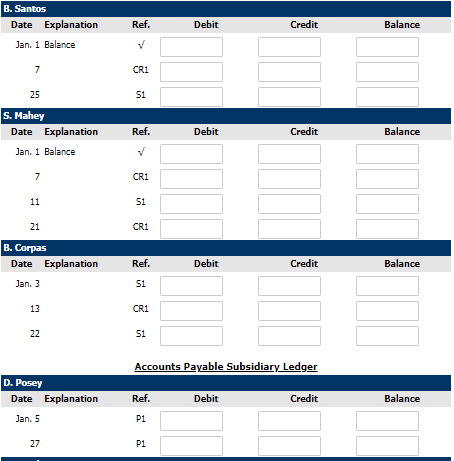

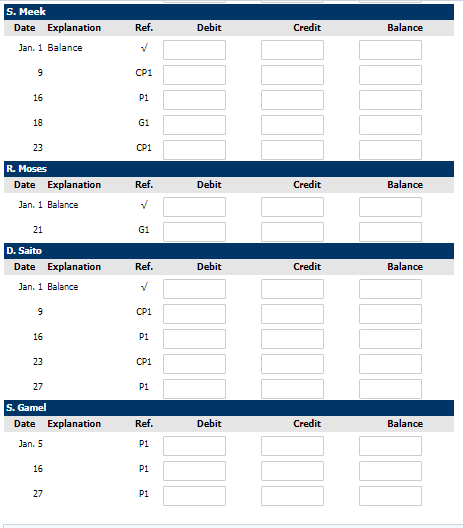

Crane Co. uses a perpetual inventory system and both an accounts receivable and an accounts payable subsidiary ledger. Balances related to both the general ledger and the subsidiary ledger for Crane are indicated in the working papers. Presented below are a series of transactions for Crane Co. for the month of January. Credit sales terms are 2/10, n/30. The cost of all merchandise sold was 60% of the sales price. Account Number 101 Cash 112 Accounts Receivable 115. Notes Receivable 120 126 130 157 Equipment 158 Accumulated Depreciation-Equip. GENERAL LEDGER 201 Accounts Payable 301 Owner's Capital Customer R. Beltre B. Santos S. Mahay Inventory Supplies Prepaid Insurance Schedule of Accounts Receivable (from accounts receivable subsidiary ledger) Account Title Customer S. Meek R. Moses D. Saito Schedule of Accounts Payable (from accounts payable subsidiary ledger) January 1 Opening Balance January 1 Opening Balance January 1 Opening Balance $1,700 7,600 3,700 $7,500 12,000 7,000 $36,750 13,000 38,000 20,000 1,600 1,700 7,350 1,500 26,500 90,400 Jan. 3 MIN 5 7 8 9 9 10 11 12 13 15 15 16 17 18 20 21 21 22 22 23 25 27 27 28 31 31 Sell merchandise on account to B. Corpas $3,800, invoice no. 510, and to J. Revere $1,500, invoice no. 511. Purchase merchandise from S. Gamel $6,000 and D. Posey $2,600, terms n/30. Receive checks from S. Mahay $3,700 and B. Santos $2,000 after discount period has lapsed. Pay freight on merchandise purchased $220. Send checks to S. Meek for $7,500 less 2% cash discount, and to D. Saito for $7,000 less 1% cash discount. Issue credit of $300 to J. Revere for merchandise returned. Daily cash sales from January 1 to January 10 total $16,500. Make one journal entry for these sales. Sell merchandise on account to R. Beltre $1,800, invoice no. 512, and to S. Mahay $900, invoice no. 513. Pay rent of $2,000 for January. Receive payment in full from B. Corpas and J. Revere less cash discounts. Withdraw $800 cash by M. Crane for personal use. Post all entries to the subsidiary ledgers. Purchase merchandise from D. Saito $16,000, terms 1/10, n/30; S. Meek $14,200, terms 2/10, n/30; and S. Gamel $1,400, terms n/30. Pay $600 cash for office supplies. Return $300 of merchandise to S. Meek and receive credit. Daily cash sales from January 11 to January 20 total $21,100. Make one journal entry for these sales. Issue $12,000 note, maturing in 90 days, to R. Moses in payment of balance due. Receive payment in full from S. Mahay less cash discount. Sell merchandise on account to B. Corpas $2,500, invoice no. 514, and to R. Beltre $2,500, invoice no. 515. Post all entries to the subsidiary ledgers. Send checks to D. Saito and S. Meek in full payment less cash discounts. Sell merchandise on account to B. Santos $3,800, invoice no. 516, and to J. Revere $6,500, invoice no. 517. Purchase merchandise from D. Saito $14,700, terms 1/10, n/30; D. Posey $3,400, terms n/30; and S. Gamel $5,700, terms n/30. Post all entries to the subsidiary ledgers. Pay $200 cash for office supplies. Daily cash sales from January 21 to January 31 total $24,000. Make one journal entry for these sales. Pay sales salaries $4,100 and office salaries $3,000. 4 56 5 Date Account Debited 3-Jan B Corpas 7 3-Jan J.Revere 8 11-Jan R.Beltre 9 11-Jan S.Mahay B Corpas 10 22-Jan 11 22-Jan R.Beltre 12 25-Jan B.Santos 13 25-Jan J.Revere 14 31-Jan Totals 15 Invoice No. 510 511 512 513 514 515 516 517 Sales Journal Post Ref Accounts Receivable - Sold - DR Sales - CR DR Cost of Goods 3,800 1,500 1,800 900 2,500 2,500 3,800 6,500 23,300 Inventory - CR 2,280 900 1,080 540 1,500 1,500 2,280 3,900 13,980 17 18 19 20 21 22 23 24 25 26 27 28 29 Date Account Credited 5-Jan S.Gamel 5-Jan D. Posey 16-Jan D.Saito 16-Jan S.Meek 16-Jan S.Gamel 27-Jan D.Saito 27-Jan D. Posey 27-Jan S.Gamel Total Purchases Journal n/30 n/30 Terms 1/10,n/30 2/10,n/30 n/30 1/10,n/30 n/30 n/30 Ref. Inventory Dr. Accounts Payable Cr. 6,000 2,600 16,000 14,200 1,400 14,700 3,400 5,700 64,000 31 32 Date Account Credited 33 34 35 36 37 38 39 40 41 42 43 44 7-Jan S. Mahay 7-Jan B. Santos 10-Jan Cash sales 13-Jan B. Corp. 13-Jan J. Revere 20-Jan Sales 21-Jan S. Mahay 31-Jan Sales Total Cash Receipts Journal Post ref. Cash Dr. 3,700 2,000 16,500 3,724 1,470 21,100 882 24,000 73,376 Sales Discount Dr. 76 30 18 124 Accounts Receivable Cr. 3,700 2,000 3,800 1,500 900 11,900 Sales Revenue Cr. 16,500 21,100 24,000 61,600 Other Accounts Cr. COGS Dr. Inventory Cr. 9,900 12,660 14,400 36,960 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 Date Account Debited 8-Jan Freight 9-Jan S.Meek 9-Jan D. Saito 12-Jan Rent 15-Jan Drawings 17-Jan Supplies 23-Jan D. Saito 23-Jan S.Meek 28-Jan Supplies 31-Jan Sales salaries 31-Jan Office salaries Total Cash Payment Journal Post ref. 120 729 306 627 Ref. Other Accounts Dr. 220 2,000 800 4,100 3,000 10,120 Accounts Payable Dr. 7,500 7,000 16,000 14,200 44,700 Supplies Dr. 600 200 800 Inventory Cr. 150 70 160 284 664 Cash Cr. 220 7,350 6,930 2,000 800 600 15,840 13,916 200 4,100 3,000 54,956 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 General Journal Date Account Title 9-Jan Sales return & allowances Accounts receivable (J. Revere) (To record credit for merchandise returned) Inventory Cost of goods Sold (To record cost of merchandise returned) 18-Jan Accounts Payable (S. Meek) Inventory (Received credit for goods returned) 21-Jan Accounts payable (R. Moses) Notes payable (Payment of balance due) Debit 220 132 300 12000 Credit 300 132 300 12000 Post the journals to the general ledger. (Post entries in the order of Journal entry presented in the previous parts.) General Ledger Cash Date Explanation Jan. 1 Balance 31 31 Accounts Receivable Date Explanation Jan. 1 Balance 31 31 9 Notes Receivable Date Explanation Jan. 1 Balance Ref. CR1 CP1 Ref. > S1 CR1 G1 Ref. Debit Debit Debit Credit Credit Credit No. 101 Balance No. 112 Balance No. 115 Balance Inventory Date Supplies Jan. 1 Balance Date 31 31 31 Equipment Date 8 31 9 Explanation 18 Explanation Jan. 1 Balance 31 Prepaid Insurance Date Explanation Jan. 1 Balance Explanation Jan. 1 Balance Accumulated Deprecia -Equipment Date Explanation Jan. 1 Balance Ref. P1 S1 CR1 CP1 CP1 G1 G1 Ref. > CP1 Ref. Ref. Ref. Debit Debit Debit Debit Debit Credit Credit Credit Credit Credit No. 120 Balance No. 125 Balance No. 130 Balance No. 157 Balance No. 158 Balance Notes Payable Date Jan. 21 Accounts Payable Date Explanation Jan. 1 Balance 31 31 18 Explanation 21 Owner's Capital Date Explanation Jan. 1 Balance Owner's Drawings Date Jan 15 Sales Revenue Date Jan. 31 Explanation Explanation 31 Sales Returns and Allowances Date Explanation Jan. 9 Sales Discounts Date Explanation Jan. 31 Ref. G1 Ref. P1 CP1 G1 G1 Ref. V Ref. CP1 Ref. S1 CR1 Ref. G1 Ref. CR1 Debit Debit Debit Debit Debit Debit Debit Credit Credit Credit Credit Credit Credit Credit No. 200 Balance No. 201 Balance No. 301 Balance No. 306 Balance No, 401 Balance No. 412 Balance No. 414 Balance Cost of Goods Sold Date Jan. 31 Jan. 9 Salaries and Wages Expense Date Explanation Rent Expense Date 31 Jan. 12 11 31 9 R. Beltre Date Explanation Jan. 1 Balance 13 Explanation 25 22 J. Revere Date Explanation Jan. 3 Explanation Ref. 51 51 Ref. 51 G1 CR1 Ref. S1 51 CR1 G1 Ref. CP1 Ref. CP1 Accounts Receivable Subsidiary Ledger Debit Debit Debit Debit Debit Credit Credit Credit Credit Credit No. 505 Balance No. 627 Balance No. 729 Balance Balance Balance B. Santos Date Explanation Jan. 1 Balance 7 25 S. Mahey Date Explanation Jan. 1 Balance 7 11 21 B. Corpas Date Explanation Jan. 3 13 22 D. Posey Date Explanation Jan. 5 27 Ref. CR1 51 Ref. CR1 51 CR1 Ref. 51 CR1 51 Ref. P1 Debit P1 Debit Debit Credit Debit Credit Accounts Payable Subsidiary Ledger 00 Credit Credit Balance Balance 0000 Balance Balance S. Meek Date Explanation Jan. 1 Balance 9 16 18 23 R. Moses Date Explanation Jan. 1 Balance 21 D. Saito Date Explanation Jan. 1 Balance 9 16 23 27 S. Gamel Date Explanation Jan. 5 16 27 Ref. CP1 P1 G1 CP1 Ref. G1 Ref. CP1 P1 CP1 P1 Ref. P1 P1 P1 Debit Debit Debit Debit Credit Credit Credit Credit Balance Balance Balance Balance

Step by Step Solution

3.44 Rating (160 Votes )

There are 3 Steps involved in it

4 5 Date 6 7 8 9 10 11 12 13 14 15 17 18 19 20 21 22 23 24 25 26 27 28 29 31 32 33 34 35 36 37 38 39 ... View full answer

Get step-by-step solutions from verified subject matter experts