Question: Create auditing proposal presentation with your financial analysis and recommendations . Include speaker notes as if you were presenting this in person. Use the Excel

Create auditing proposal presentation with your financial analysis and recommendations. Include speaker notes as if you were presenting this in person. Use the Excel template Create a auditing proposal presentation with your financial analysis and recommendations. Include speaker notes as if you were presenting this in person. Use the Excel template provided to track your calculation and add visuals to your presentation.

Include the following items in your auditing proposal:

Include the following items in your auditing proposal:

Background & Operational Structure:

Describe thehealth care organization.

Include the history and purpose; identify the service or product they offer.

This information is typically found in the annual report.

Describe the company's operational structure (e.g., sole-proprietorship, corporation, partnership).

Financial Analysis and Stability:

Explain the purpose of financial analysis.

Describe the 3 basic tools of financial analysis (vertical, horizontal, and financial ratios).

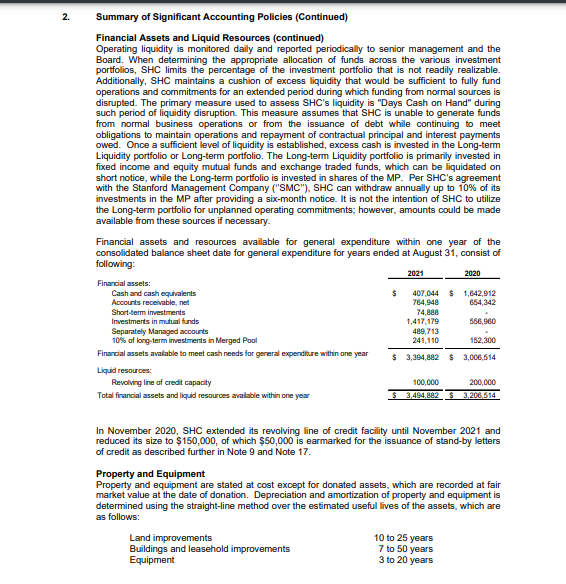

2. Summary of Significant Accounting Policies (Continued) Financial Assets and Liquid Resources (continued) Operating liquidity is monitored daily and reported periodically to senior management and the Board. When determining the appropriate allocation of funds across the various investment portfolios, SHC limits the percentage of the investment portfolio that is not readily realizable. Additionally, SHC maintains a cushion of excess liquidity that would be sufficient to fully fund operations and commitments for an extended period during which funding from normal sources is disrupted. The primary measure used to assess SHC's liquidity is "Days Cash on Hand" during such period of liquidity disruption. This measure assumes that SHC is unable to generate funds from normal business operations or from the issuance of debt while continuing to meet obligations to maintain operations and repayment of contractual principal and interest payments owed. Once a sufficient level of liquidity is established, excess cash is invested in the Long-term Liquidity portfolio or Long-term portfolio. The Long-term Liquidity portfolio is primarily invested in fixed income and equity mutual funds and exchange traded funds, which can be liquidated on short notice, while the Long-term portfolio is invested in shares of the MP. Per SHC's agreement with the Stanford Management Company ("SMC"), SHC can withdraw annually up to 10% of its investments in the MP after providing a six-month notice. It is not the intention of SHC to utilize the Long-term portfolio for unplanned operating commitments; however, amounts could be made available from these sources if necessary. Financial assets and resources available for general expenditure within one year of the consolidated balance sheet date for general expenditure for years ended at August 31, consist of following: 2021 2020 Financial assets: Cash and cash equivalents 407,044 $ 1,642,912 Accounts receivable, net 784,940 684,142 Short-term investments 74, BOU Investments in mutual funds 1,417,179 Separately Managed accounts 489,713 10% of long-term investments in Merged Pool 241,110 182, 200 Financial assets available to meet cash needs for general expenditure within one year $ 3,394,842 $ 3,006,614 Liquid resources: Revolving line of credit capacity 100,000 200,000 Total financial assets and liquid resources available within one year 3,494 812 3,206,614 In November 2020, SHC extended its revolving line of credit facility until November 2021 and reduced its size to $150,000, of which $50,000 is earmarked for the issuance of stand-by letters of credit as described further in Note 9 and Note 17. Property and Equipment Property and equipment are stated at cost except for donated assets, which are recorded at fair market value at the date of donation. Depreciation and amortization of property and equipment is determined using the straight-line method over the estimated useful lives of the assets, which are as follows: Land improvements 10 to 25 years Buildings and leasehold improvements 7 to 50 years Equipment 3 to 20 years

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!