Question: Credit risk measures using the structural model: assume a company has the following characteristics. Time t value of the firms asset: At = $2,000 Expected

Credit risk measures using the structural model: assume a company has the following characteristics.

Time t value of the firms asset: At = $2,000

Expected return on assets: u = 0.06 per year

Risk-free rate: r = 0.03 per year

Face value of the firms debt: K = $1,500

Time to maturity of the debt (tenor): T t = 0.5 year

Asset return volatility: = 0.30 per year

(a) Calculate the probability that the debt will default over the time to maturity.

(b) Calculate the expected loss.

(c) Calculate the present value of the expected loss.

show all calculations All prices and interest rates must be expressed to three decimal places

I have added an example question below the way the professor wants his answers to be.

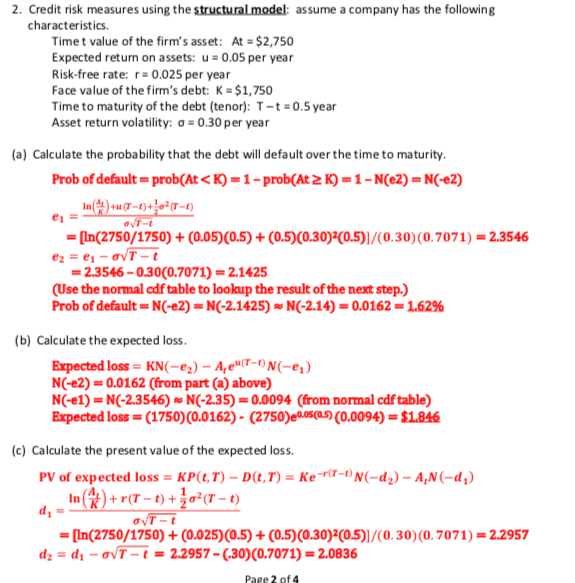

VT- 2. Credit risk measures using the structural model: assume a company has the following characteristics Timet value of the firm's asset: At = $2,750 Expected return on assets: u = 0.05 per year Risk-free rate: r = 0.025 per year Face value of the firm's debt: K = $1,750 Time to maturity of the debt (tenor): T-t = 0.5 year Asset return volatility: 0 = 0.30 per year (a) Calculate the probability that the debt will default over the time to maturity. Prob of default = prob(At

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts