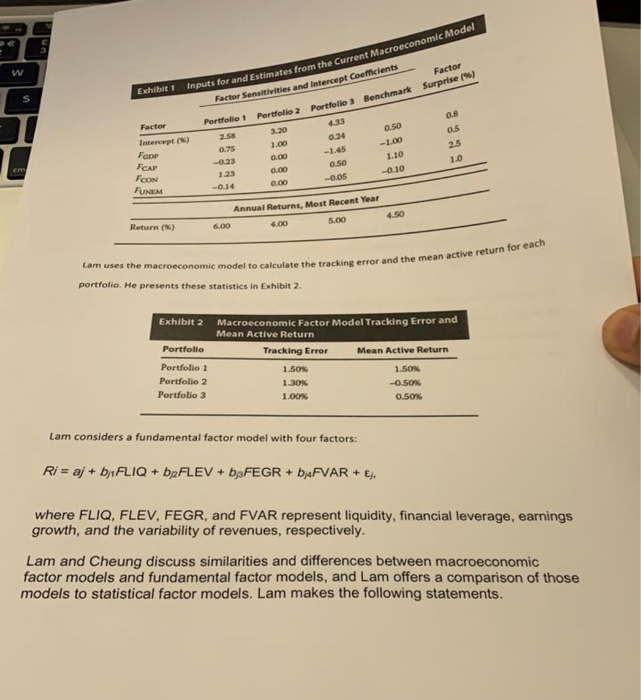

Question: Current Macroeconomic Model W Factor Surprise inputs for and Estimates from the Current Macro Exhibit 1 Factor Sensitivities and Intercept Coefficients Benchmark Portfolio 3 Portfolio

Current Macroeconomic Model W Factor Surprise inputs for and Estimates from the Current Macro Exhibit 1 Factor Sensitivities and Intercept Coefficients Benchmark Portfolio 3 Portfolio 2 0.8 Factor Portfolio 4.33 05 0.24 2.58 0.75 Intercept() 3.30 1.00 0.00 0.50 -1.00 1.10 FGOP FCAP FOON -1.45 0.50 -0.05 0.00 -0.10 0.00 FUNEM -0.14 Annual Returns, Most Recent Year 4.50 Return () 6.00 6.00 4.00 4. 00 .00 5 the macroeconomic model to calculate the tracking error and the mean active ror and the mean active return for each portfolio. He presents these statistics in Exhibit 2. Exhibit 2 Portfolio Portfolio 1 Portfolio 2 Portfolio 3 Macroeconomic Factor Model Tracking Error and Mean Active Return Tracking Error Mean Active Return 1.50% 1.50% 1.30% -0.50 1.00% 0.50% Lam considers a fundamental factor model with four factors: Ri= aj + b1FLIQ + b2FLEV + DFEGR + b/FVAR + E). where FLIQ, FLEV, FEGR, and FVAR represent liquidity, financial leverage, earnings growth, and the variability of revenues, respectively. Lam and Cheung discuss similarities and differences between macroeconomic factor models and fundamental factor models, and Lam offers a comparison of those models to statistical factor models. Lam makes the following statements. Current Macroeconomic Model W Factor Surprise inputs for and Estimates from the Current Macro Exhibit 1 Factor Sensitivities and Intercept Coefficients Benchmark Portfolio 3 Portfolio 2 0.8 Factor Portfolio 4.33 05 0.24 2.58 0.75 Intercept() 3.30 1.00 0.00 0.50 -1.00 1.10 FGOP FCAP FOON -1.45 0.50 -0.05 0.00 -0.10 0.00 FUNEM -0.14 Annual Returns, Most Recent Year 4.50 Return () 6.00 6.00 4.00 4. 00 .00 5 the macroeconomic model to calculate the tracking error and the mean active ror and the mean active return for each portfolio. He presents these statistics in Exhibit 2. Exhibit 2 Portfolio Portfolio 1 Portfolio 2 Portfolio 3 Macroeconomic Factor Model Tracking Error and Mean Active Return Tracking Error Mean Active Return 1.50% 1.50% 1.30% -0.50 1.00% 0.50% Lam considers a fundamental factor model with four factors: Ri= aj + b1FLIQ + b2FLEV + DFEGR + b/FVAR + E). where FLIQ, FLEV, FEGR, and FVAR represent liquidity, financial leverage, earnings growth, and the variability of revenues, respectively. Lam and Cheung discuss similarities and differences between macroeconomic factor models and fundamental factor models, and Lam offers a comparison of those models to statistical factor models. Lam makes the following statements

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts