Question: D Pregunta 18 h The following represents two yield curves. Maturity Treasuries Corporate 6 months 2% 3% 1 year 3% 4% 5 years 4% 5%

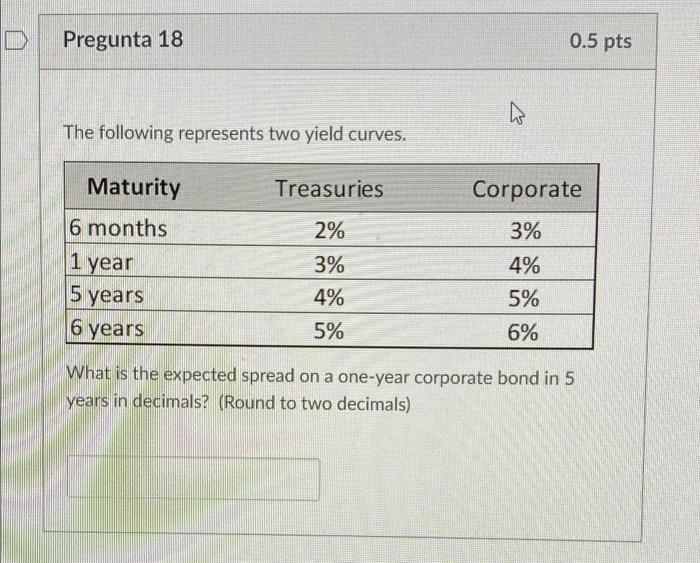

D Pregunta 18 h The following represents two yield curves. Maturity Treasuries Corporate 6 months 2% 3% 1 year 3% 4% 5 years 4% 5% 6 years 5% 6% What is the expected spread on a one-year corporate bond in 5 years in decimals? (Round to two decimals) 0.5 pts

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock