Question: D | Question 4 1 pts Questions 1-4 are based on the following information: A U.S. firm holds an asset in France and considers selling

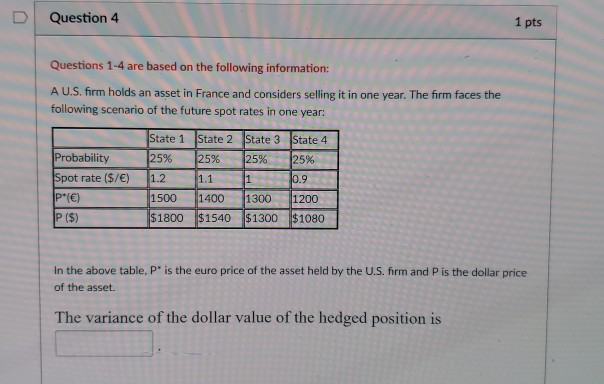

D | Question 4 1 pts Questions 1-4 are based on the following information: A U.S. firm holds an asset in France and considers selling it in one year. The firm faces the following scenario of the future spot rates in one year: State 2 State 3 State 4 State 1 Probability 125% 125% 125% 125% Spot rate (S/) 1.2 1.1 15001400 1300 1200 P ($) $1800 $1540 $1300 $1080 In the above table, P" is the euro price of the asset held by the U.S. firm and P is the dollar price of the asset. The variance of the dollar value of the hedged position is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock