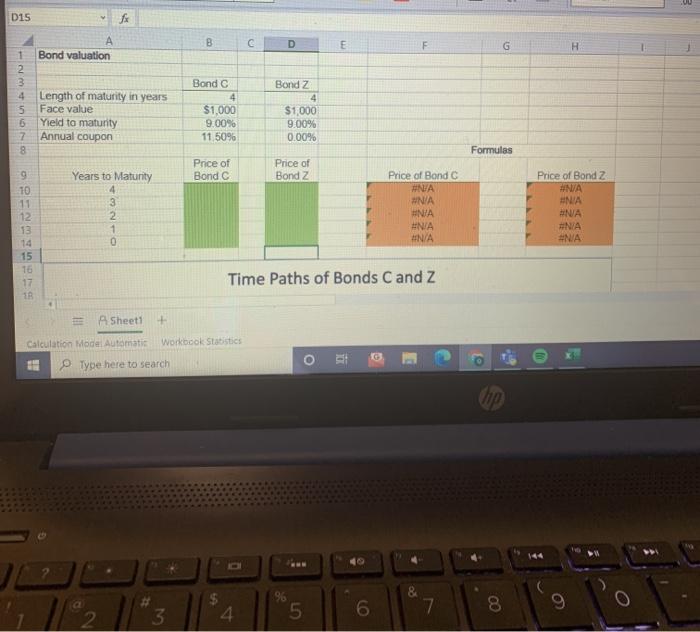

Question: D15 fx B A Bond valuation D E G H 1 2 3 4 5 Length of maturity in years Face value Yield to maturity

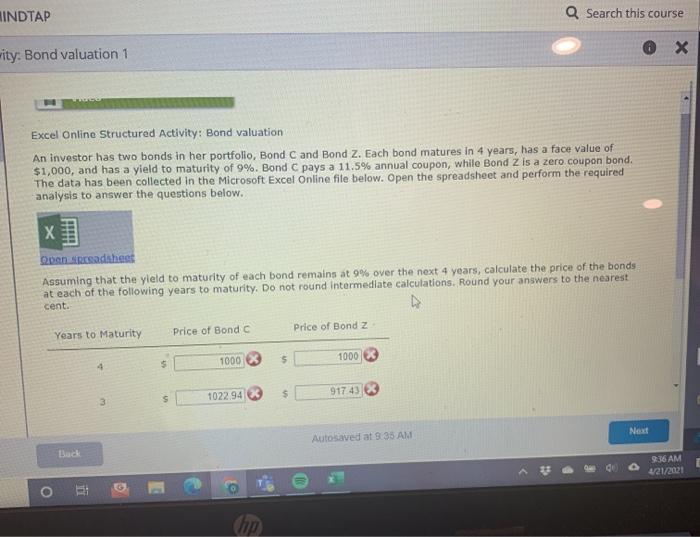

D15 fx B A Bond valuation D E G H 1 2 3 4 5 Length of maturity in years Face value Yield to maturity Annual coupon Bond C 4 $1,000 9.00% 11 50% Bond Z 4. $1,000 9.00% 0.00% Formulas Price of Bond C Price of Bond z 9 10 11 12 13 14 15 TO 17 1 Years to Maturity 4 3 2 1 0 Price of Bond C #NA #N/A #N/A #N/A N/A Price of Bond Z #N/A NA NA #N/A #NA Time Paths of Bonds C and Z . A Sheet1 + Calculation Model Automatic Workbook Statistics Type here to search 96 5 & 7 6 8 2 3 4 INDTAP Search this course wity: Bond valuation 1 X Excel Online Structured Activity: Bond valuation An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the questions below. HHH Qan pesadahen Assuming that the yield to maturity of each bond remains at 9% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Do not round intermediate calculations. Round your answers to the nearest cent. Years to Maturity Price of Bond C Price of Bond Z $ 1000 5 1000 1022 94 s 3 91743 Next AutoSaved at 9:35 AM Buck 9:36 AM 4/21/2021

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts