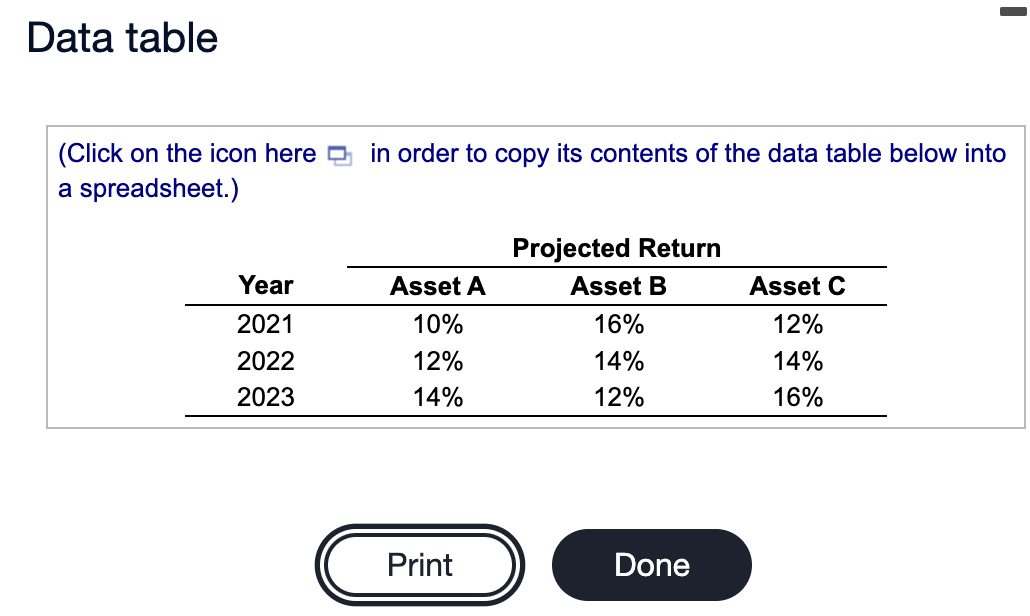

Question: - Data table (Click on the icon here e in order to copy its contents of the data table below into a spreadsheet.) Asset A

- Data table (Click on the icon here e in order to copy its contents of the data table below into a spreadsheet.) Asset A Year 2021 2022 2023 10% 12% 14% Projected Return Asset B 16% 14% 12% Asset C 12% 14% 16% Print Done You have been asked for your advice in selecting a portfolio of assets and have been supplied with the following data: You have been told that you can create two portfoliosone consisting of assets A and B and the other consisting of assets A and Cby investing equal proportions (50%) in each of the two component assets. a. What is the average expected return, r, for each asset over the 3-year period? b. What is the standard deviation, s, for each asset's expected return? c. What is the average expected return, rp, for each of the the portfolios? d. How would you characterize the correlations of returns of the two assets making up each of the portfolios identified in part c? e. What is the standard deviation of expected returns, Sp, for each portfolio? f. Which portfolio do you recommend? Why? ... a. What is the average expected return, r, for each asset over the 3-year period? Asset A: % (Round to one decimal place.) Asset B: % (Round to one decimal place.) Asset C: % (Round to one decimal place.) b. What is the standard deviation, s, for each asset's expected return? Asset A: % (Round to two decimal places.) Asset B: % (Round to two decimal places.) Asset C: % (Round to two decimal places.) c. What is the average expected return, in, for each of the two portfolios? Portfolio AB: % (Round to one decimal place.) Portfolio AC: % (Round to one decimal place.) d. How would you characterize the correlations of returns of the 2 assets making up each of the 2 portfolios identified in part c? Portfolio AB is perfectly correlated, while Portfolio AC is perfectly correlated. (Select from the drop-down menus.) e. What is the standard deviation of expected returns, Sp, for each portfolio? Portfolio AB: % (Round to two decimal places.) Portfolio AC: % (Round to two decimal places.) f. Which portfolio do you recommend? Why? (Select the best choice below.) A. Portfolio AC is preferred since it provides greater return than Portfolio AB but with more risk, as measured by the standard deviation. B. Portfolio AB is preferred since it provides the same return as Portfolio AC but with less risk, as measured by the standard deviation. C. Portfolio AB is preferred since it provides greater return than Portfolio AC but with more risk, as measured by the standard deviation. OD. Portfolio AC is preferred since it provides the same return as Portfolio AB but with less risk, as measured by the standard deviation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts